Sustainable Governance Operation Mechanisms >

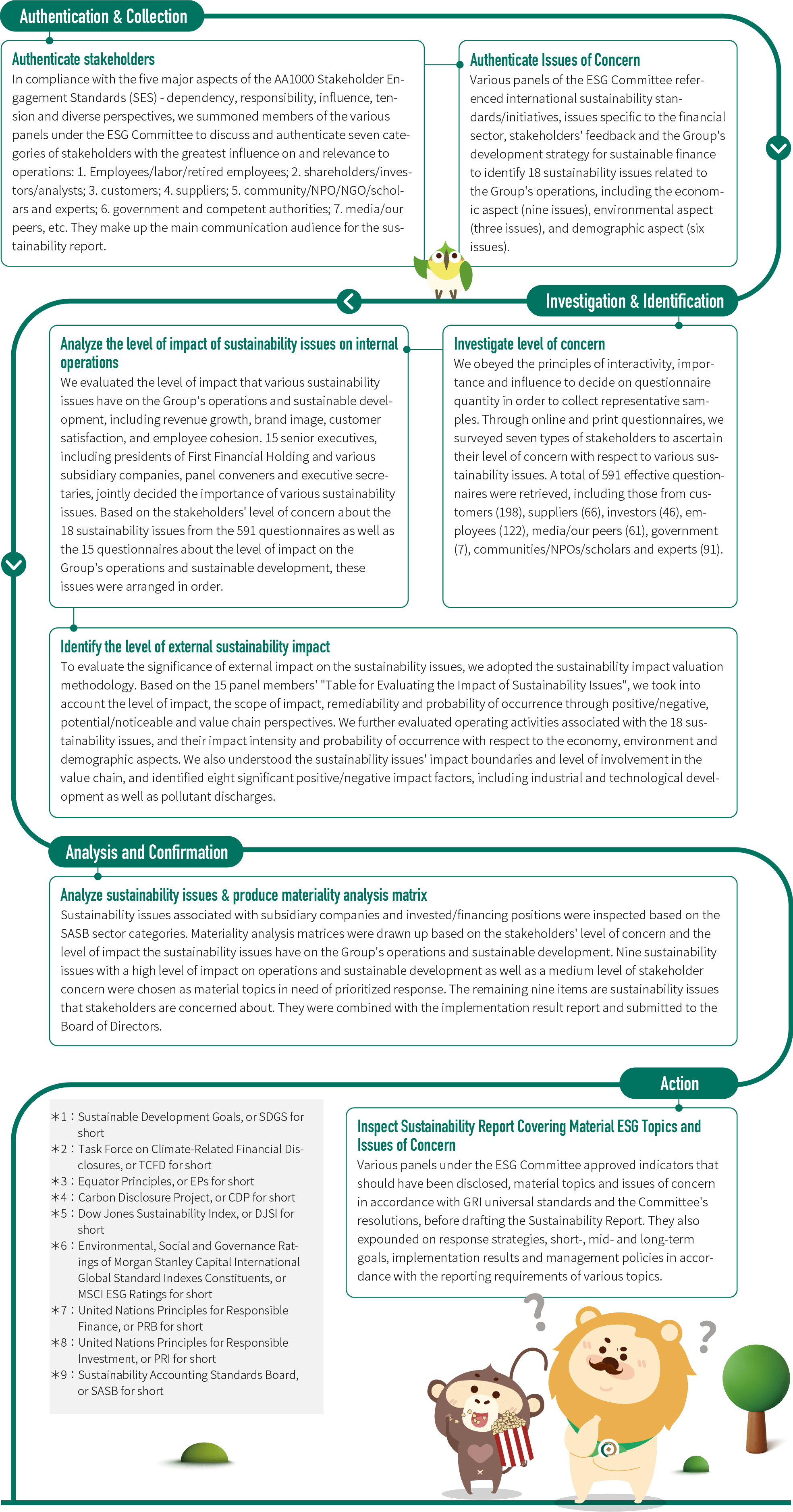

Stakeholder Communication and Materiality Assessment Process

Stakeholder Communication and Materiality Assessment Process

Stakeholder identification and communication

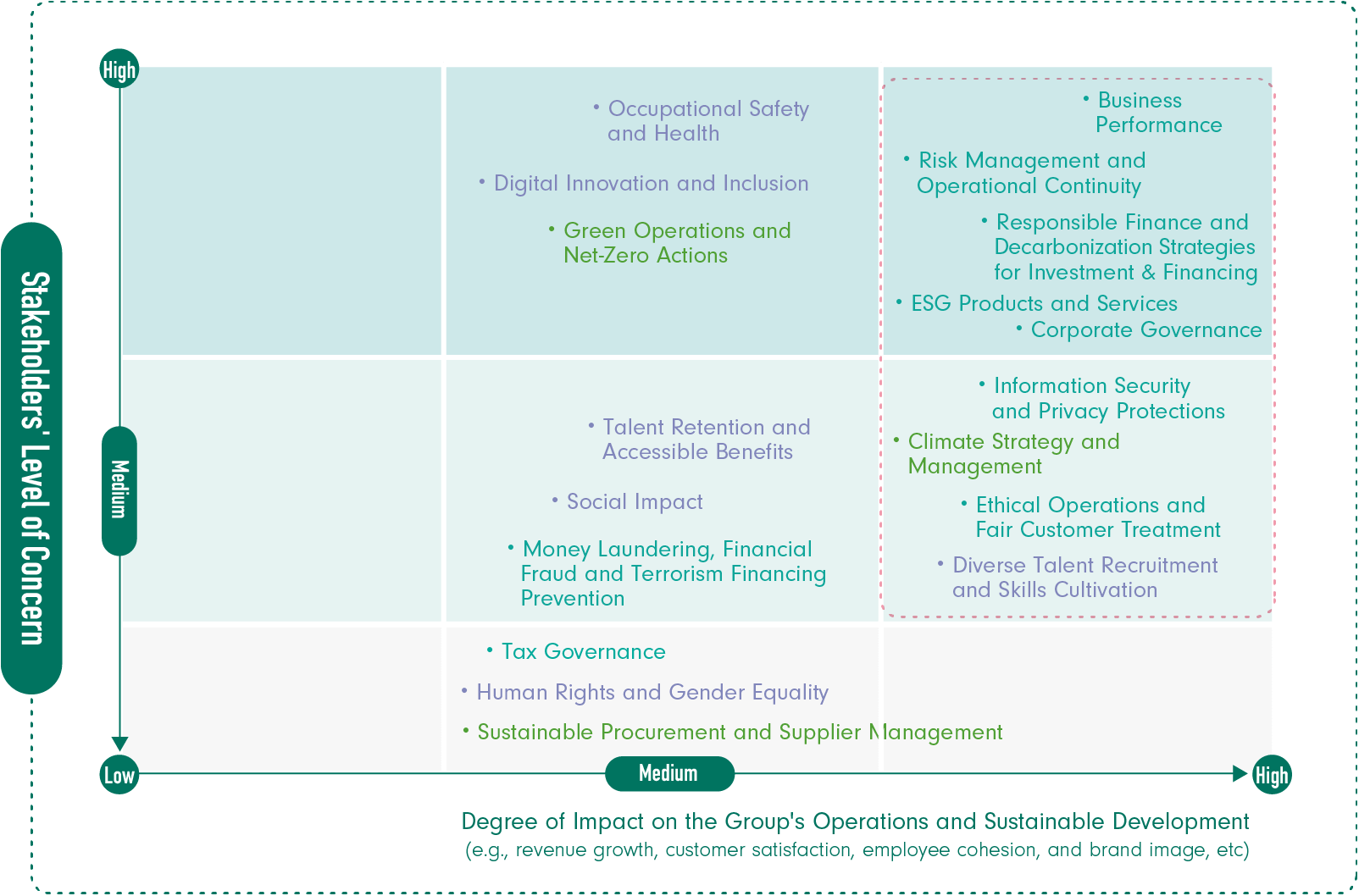

Since publishing its 2011 Sustainability Report in 2012, First Financial Holding has demonstrated its long-standing commitment to sustainable management and information disclosure. We also view stakeholders' comments and feedback as important basis for formulating our sustainable development strategy. We actively listen and respond to stakeholders' demands and expectations, in order to ensure that the content of our reports are highly relevant and responsive. During the course of identifying material topics, First Financial Holding took a deep dive to understand stakeholders' concerns and focus on environmental, social and governance (ESG) issues. We also referenced international sustainability standards and initiatives, such as the GRI Standards, ISO 26000, SDGs*1, TCFD*2, and the Equator Principles*3; International sustainability ratings such as CDP*4, DJSI*5, MSCI ESG Ratings*6, the financial sector's specific issues PRB*7, PRI*8, SASB*9, GRI industrial disclosure index for the financial services industry, communication with stakeholders and their feedback, integrated international sustainability disclosure standards, and the Group's development strategy for sustainable finance serve as the basis for analyzing material topics. To further respond to GRI 2021 Universal Standards G3: Material Topics 2021, the Group integrated the impact assessment methodology, which encompasses the economy, environment and demographics (including human rights) aspects and was developed by institutions including the Value Balancing Alliance (VBA), Harvard Business School's Impact-Weighted Accounts Project and London Benchmarking Group (LBG). We also incorporated the Double Materiality approach recommended by the European Financial Reporting Advisory Group (EFRAG), and adopted the monetization and non-monetization methodologies to build an analysis flow encompassing impact and financial materiality (four major stages and seven major steps). Taking both the "organizational operation impact" and "economy, environment and people/demographic impact" into account, we evaluated the impact of sustainability issues from perspectives inside and outside the organization, respectively. By doing so, we were able to identify nine material topics with substantive and positive/negative impact on economy, environment and demographics (including human rights). These are the material topics we prioritized for response. The other nine are sustainability issues that stakeholders are concerned about, and they form the basis for report drafting.

Material Topics Identification and Management

In terms of the investigation into "stakeholders' level of concern", we obeyed the principles of interactivity, importance and influence to decide on questionnaire quantity in order to collect samples with solid representation. Panel members under the ESG Committee then evaluated the "level of external impact from various issues". They then conducted scoring on various factors such as revenue, customer satisfaction level, employee cohesion, and brand image to understand key issues under different factors, before deciding on the importance of each sustainability issue as well as their order of disclosure.

Furthermore, in view of the fact that external impact on environment and society derived from corporate operations has gradually come to the attention of global investors, and in response to the revised version of GRI 2021 Universal Standards G3: Material Topics 2021, First Financial Holding has integrated the impact assessment methodology, which encompasses the economy, environment and society aspects and was developed by institutions including the Value Balancing Alliance (VBA), Harvard Business School's Impact-Weighted Accounts Project and London Benchmarking Group (LBG). We also incorporated the European Sustainability Reporting Standards (ESRS) published by the Corporate Sustainability Reporting Directive (CSRD) and the ESRS' Double Materiality concept, and adopted the monetization and non-monetization methodologies to build an analysis flow encompassing impact and financial materiality. Taking both the "organizational operation impact" and "economy, environment and demographic (including human rights)" into account, we evaluated the impact of sustainability issues from perspectives inside and outside the organization, respectively. Sustainability issues associated with subsidiary companies and invested/financing positions were inspected based on the SASB sector categories. Materiality analysis matrices were produced by referencing stakeholders' level of concern and the level of impact the sustainability issues have on the Group's operations and sustainable development. Nine material topics with a high level of impact on operations and sustainable development were identified and chosen as material topics in need of prioritized response. The remaining nine topics are sustainability issues that stakeholders are concerned about.

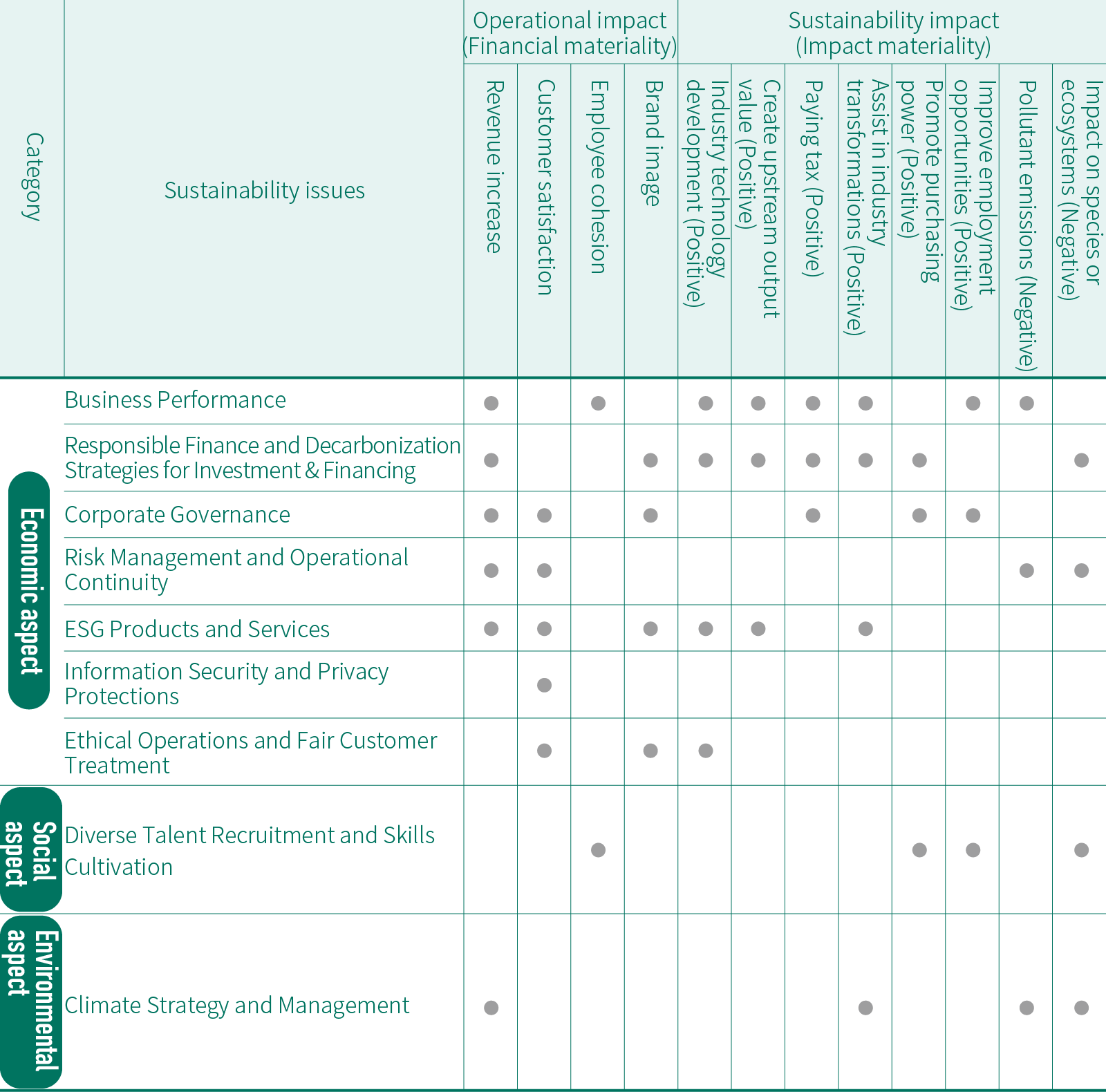

◎ Impact Evaluation on the Economy, Environment and Demographic Aspects

●:Impact Evaluation on the Economy, Environment and Demographic Aspects

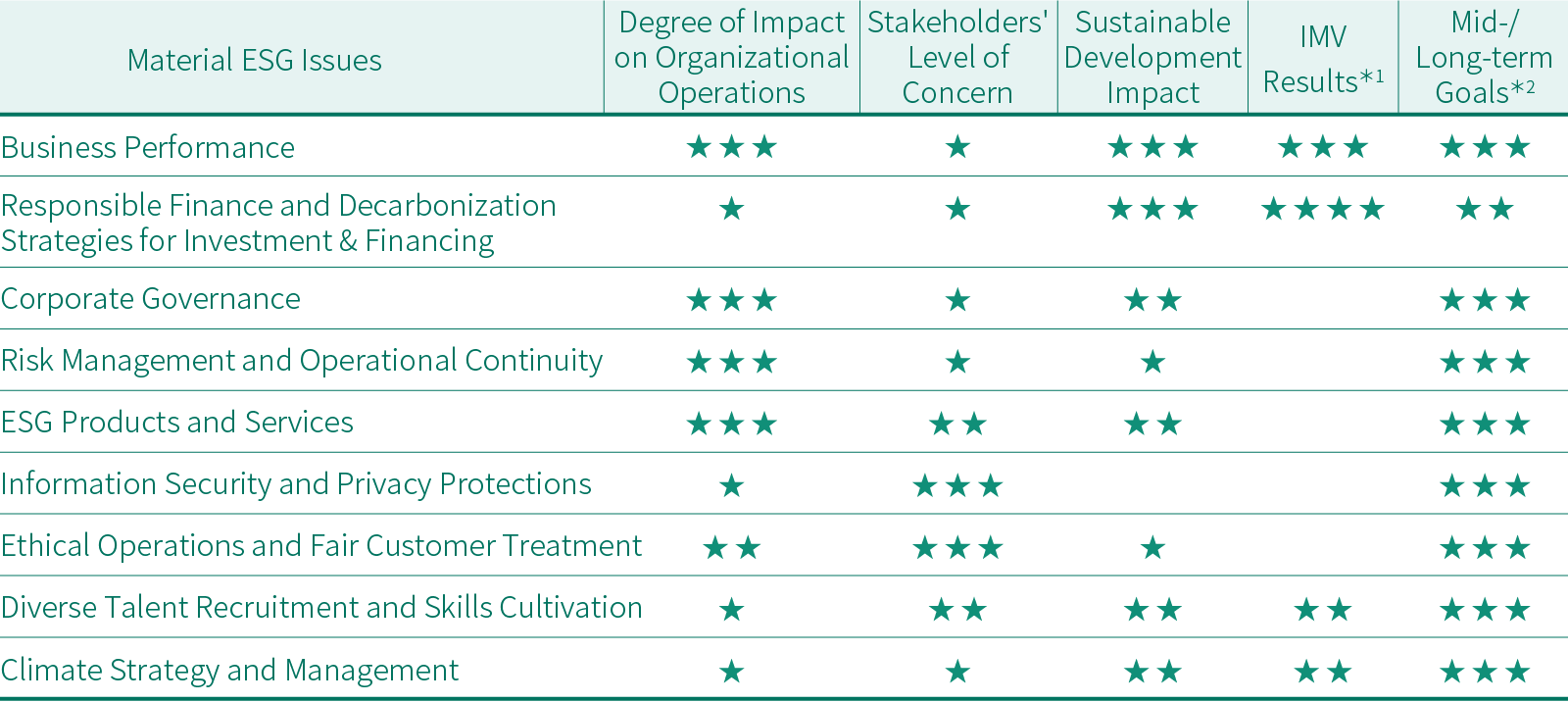

◎ Sustainability issue impact assessment results

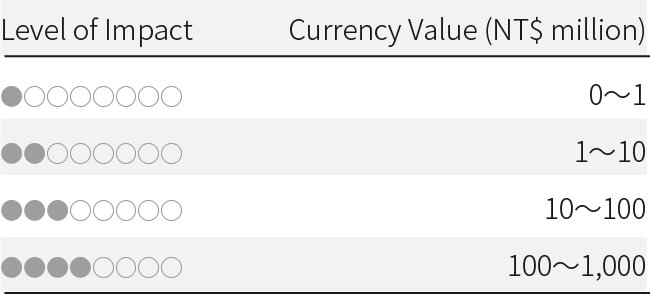

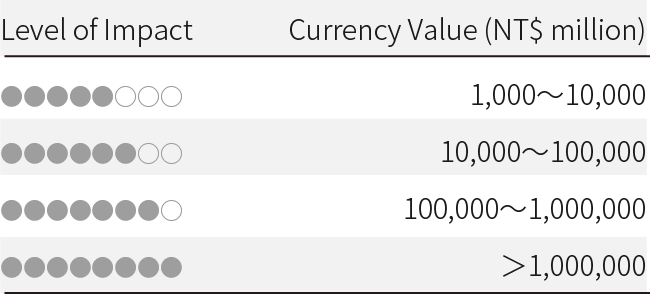

*1:「★」represents monetary value between NT$0 and 10 million;「★★」represents monetary value between NT$10 million and 1,000 million;「★★★」represents monetary value between NT$1,000 million and 100,000 million;「★★★★」represents monetary value greater than NT$100,000 million.

*2:「★」sets qualitative targets;「★★」sets one quantitative target;「★★★」sets two quantitative targets.

◎ First Financial Holding ESG matrix

Sustainable impact assessment of value chain activities

As a cash flow provider for the industry chain, First Financial Holding is extremely concerned with the impact onto society and the environment. Our management thinking linked to financial performance can identify the positive/negative, potential/significant, and mid- and long-term impact of the Group's operations towards human life. To effectively identify its external impact on economy, environment and people/human rights, First Financial Holding has combined non-monetization and monetization analyses to gain insight into the status of its external impact.

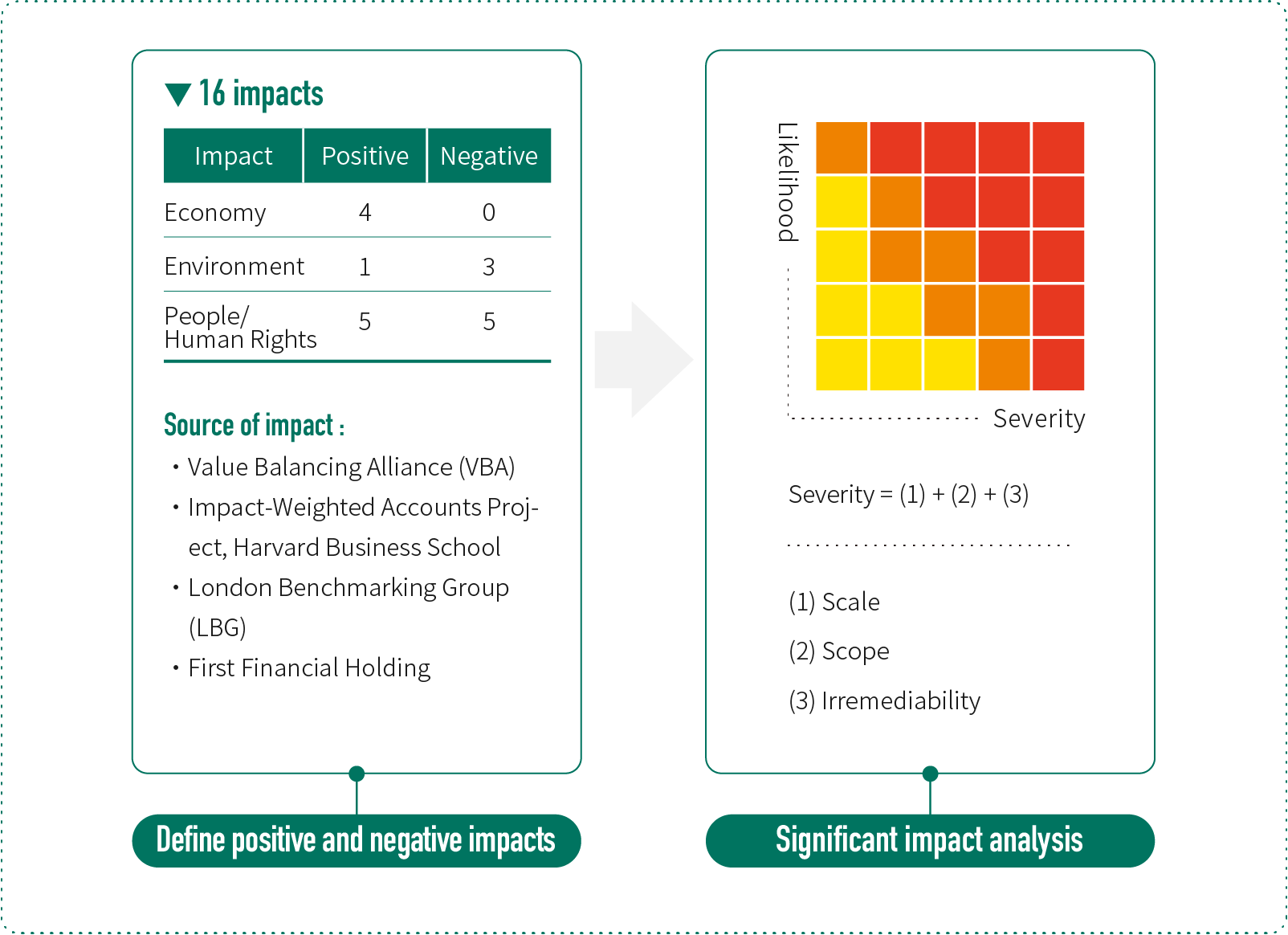

◎ Impact assessment model - non-monetization approach

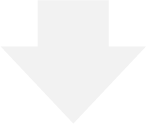

16 external impact factors relating to economy, environment and people/human rights were adopted through a survey. Taking into account their severity (including the level of impact, scope of impact and remediability) and probability of occurrence, we identified eight significant impact factors, after reaching a consensus through suggestions from external and internal experts and internal executive meetings.

These include: "positive economic aspect: R&D and innovation of company products or services conducive to the financial sector's development and applications"; "positive economic aspect: create upstream or industrial output value"; "positive economic aspect: payment of taxes or other government fees conducive to supporting infrastructure and social welfare"; "positive environmental aspect: assist industries in sustainable development or green transition through investment/credit/financial products and services"; "negative environmental aspect: presence of pollutant discharges impacting human health"; "negative environmental aspect: impact on species or ecosystems"; "positive people/human rights aspect: payment of employee remuneration conducive to purchasing power and quality of life"; and "positive people/human rights aspect: increase in employment and job opportunities leading to skills improvement". This indicates that the Group attaches great importance to the management of sustainability issues, including business performance, Responsible Finance and decarbonization strategies for investment & financing, diverse talent recruitment and skills cultivation, ESG products and services, climate and strategy management, and corporate governance.

These include: "positive economic aspect: R&D and innovation of company products or services conducive to the financial sector's development and applications"; "positive economic aspect: create upstream or industrial output value"; "positive economic aspect: payment of taxes or other government fees conducive to supporting infrastructure and social welfare"; "positive environmental aspect: assist industries in sustainable development or green transition through investment/credit/financial products and services"; "negative environmental aspect: presence of pollutant discharges impacting human health"; "negative environmental aspect: impact on species or ecosystems"; "positive people/human rights aspect: payment of employee remuneration conducive to purchasing power and quality of life"; and "positive people/human rights aspect: increase in employment and job opportunities leading to skills improvement". This indicates that the Group attaches great importance to the management of sustainability issues, including business performance, Responsible Finance and decarbonization strategies for investment & financing, diverse talent recruitment and skills cultivation, ESG products and services, climate and strategy management, and corporate governance.

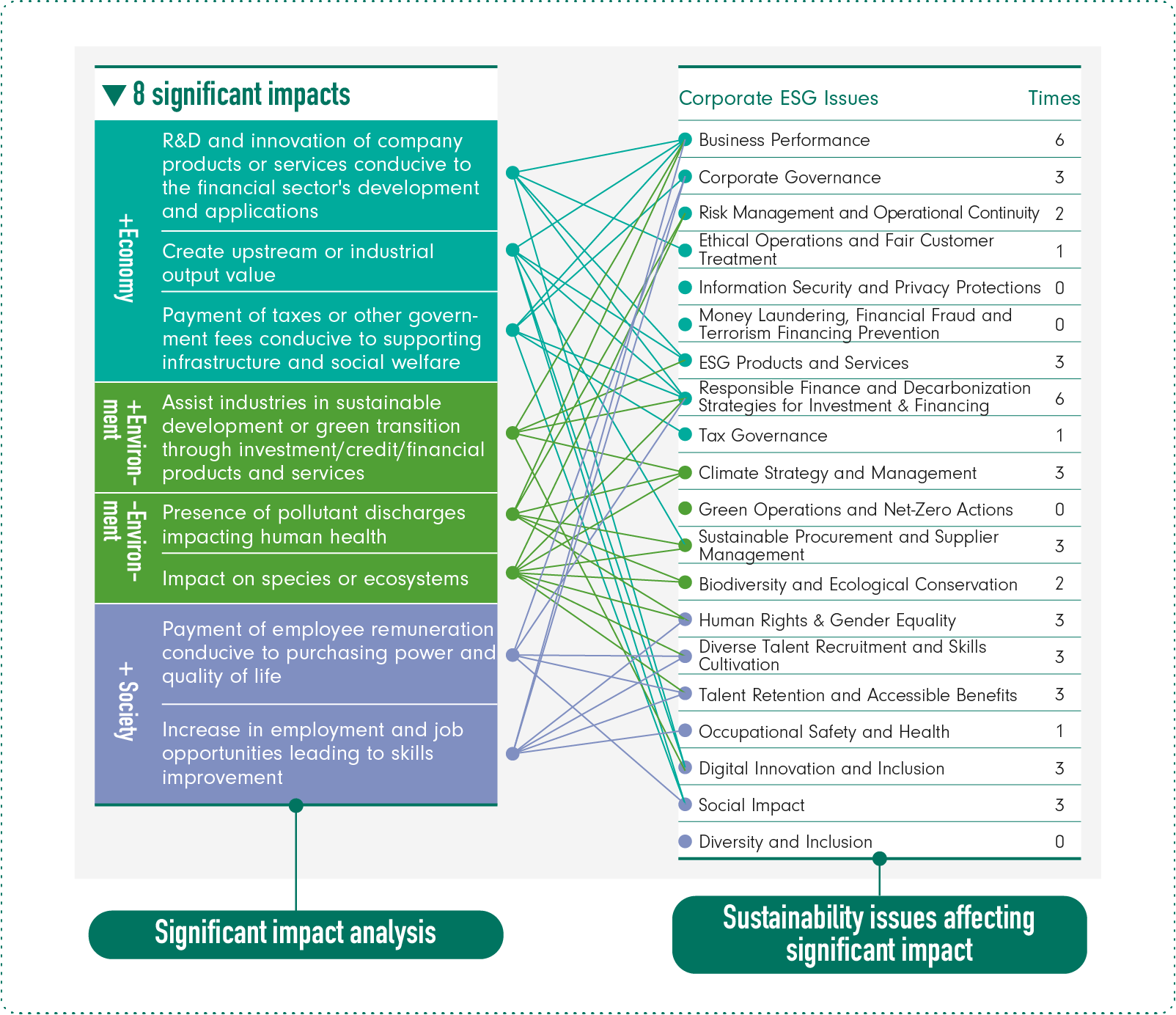

◎ Impact assessment model - monetization approach

In 2024, First Financial Holding's value chain activities created a total of NT$4.6 trillion in positive impact, while bringing about NT$59.5 billion in negative impact. In particular, more than 96% of the impact came from downstream investment and financing operations, suggesting the importance of the financial sector in driving the transition to industrial sustainability. Through investment and financing operations, First Financial Holding drove industry chains to create NT$4 trillion in output value, creating 750,000 job opportunities and NT$352.1 billion in salary income. However, natural resources consumed and environmental pollution produced in the industrial supply and demand process also derived NT$59.3 billion in social cost. In terms of positive impacts, our investments boosted industrial output, created job opportunities and salaries, after-tax net profit, interest, and employee compensation, which are considered high-impact items. Among negative impacts, high-impact items were mainly pollutant emissions caused by investments and credit. From these significant high-impact items, we can define that Responsible Finance and decarbonization strategies for investment & financing, business performance and talent retention & accessible benefits are ESG issues with relatively higher impact. In order to mitigate negative impact, First Financial Holding is dedicated to utilizing financial influence and core functions to expand the effect of sustainable investments and financing to more effectively allocate resources, support industry transitions towards sustainable development, and share sustainable values with stakeholders.

*1:Added value income includes net profit after tax (shareholders/investors), interest (customers), leasing (suppliers), compensation (employees), depreciation and amortization (suppliers), and taxes (society), which directly generate financial benefits for stakeholders. The methodology references VBA (2022).

*2:Externality refers to the positive or negative impacts on human well-being resulting from the interactions between FFHC's operational activities and various types of capital. These impacts do not directly generate benefits or costs for the company. Environmental externalities consider the carbon social cost, human health loss costs, and ecosystem damage resulting from greenhouse gases, air pollution, waste, and water resource consumption. Social externalities consider the employment impact on employees and society brought by issues such as salary quality, career development, equal opportunities, health, and well-being.

*3:In view of the differences in economic performances among various nations, valuation coefficients were adjusted to align with the gross national income (GNI) measured from the purchasing power parity (PPP) of various areas. Factors such as inflation and currency exchange rates were also taken into account, as the temporal boundary was aligned with the monetary value benchmark in 2017. OECD (2012) and PwC UK (2015) were referenced for methodology.