Economic Factors >

Risk Management and Continuous Operation

Risk Management and Continuous Operation

Our company has established internal controls in accordance with the "Implementation Rules of Internal Audit and Internal Control System of Financial Holding Companies and Banking Industries". The system covers all business activities and require joint compliance by the Board of Directors, management, and all employees. The Board of Directors shall be aware of the operational risks faced by the company or business, supervise its operating results and bears the ultimate responsibility for ensuring the establishment and maintenance of appropriate and effective internal control system.

To improve the internal control system and strengthen the Company's controls, we established three lines model in internal controls and clarified the roles and scope of duties of the three lines model to ensure the organization structure meets the principles of the three lines model and their effective operations.

First line model – Internal inspection by Business unit

Business units are responsible for identifying, evaluating, controlling, and reducing risks derived from business activities based on their respective functions and scope of businesses. We established internal control procedures and execute risk management procedures to ensure that the execution of business operations meet the business policies and goals. We also organize self-inspection and self-assessments for internal controls and immediately propose improvement plans when processes and control procedures prove to be inadequate. According to the Company's 2023 "Compliance Risk Assessment Report", which was submitted to the Board of Directors for review before being approved in June 2024, the Group reached 100% in terms of the rate of conducting corruption risk evaluation for its domestic and overseas business locations. In particular, AML and employees' related personal activities were evaluated to be medium-to-high risk. The subsidiary bank, securities company, investment trust company and life insurance company have all formulated related internal guidelines for control and management, in order to reduce the risk of corruption.

Second line model - Sound compliance and risk management system

The second line roles include the Risk Management, Compliance, and other units with related tasks (e.g. financial control, human resources, and legal affairs) which are responsible for formulating overall risk management policies for main risks, supervising overall risk-bearing capacity and current status of risks already incurred, and reporting the risk management status to the Board of Directors or senior management.

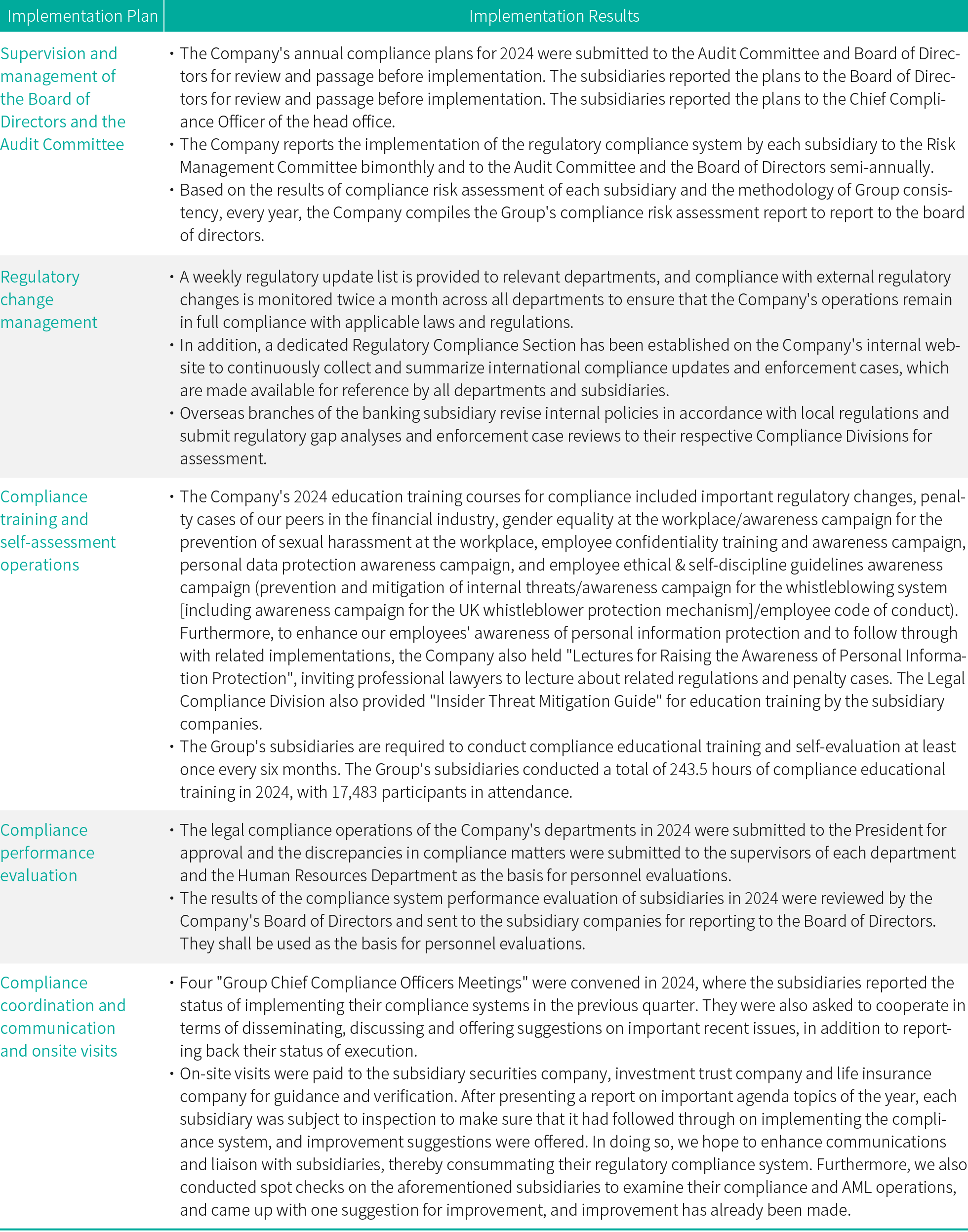

Compliance system

FFHC, First Bank, First Securities, First Securities Investment Trust and First Life Insurance have all established dedicated compliance units reporting to the president in accordance of the law. Other subsidiaries also appointed the Chief Compliance Officers at their head offices. The Chief Compliance Officers are responsible for the planning, management and execution of the regulatory compliance system at their respective companies. FFHC is continuing to require all subsidiaries to enforce their compliance systems. Related developments in 2024 are as follow:

In 2024, the Company and its subsidiaries were penalized in four cases by Taiwanese and overseas competent authorities for a total sanction amount of around NT$670,000. There were no major penalty cases*

*:The disclosure of penalties relating to cases of major violations must comply with Article 36, Paragraph 3, Item 2 of the Securities Exchange Act if there is a possible of material impact to the rights and interests of shareholders or the price of securities or if it complies with Article 2 of the "The Financial Supervisory Commission's Measures for the Public Announcement in Major Penalty Violations of Financial Laws".

Risk management

01. Risk Management Structure

FFHC's Board of Directors is the top policy-making unit when it comes to Group risk management. A "Risk Management Committee" has been established under it. The Chairman serves as the committee chairperson, while the President, VPs and the chairmen and presidents of subsidiaries serve as committee members. A meeting would be convened once every two months to supervise and examine the effectiveness and implementation status of the Group's and each subsidiary's risk management, which is reported to the Board of Directors on a regular basis. The Risk Management Department is responsible for carrying out various risk management policies.

02. Risk management Policies & Process

A.The Group identifies, weighs, monitors and controls each risk based on the "Risk Management Policy" approved by the Board of Directors, and formulates qualitative and quantitative measures commensurate with risk appetite.

・Identification of Risks: The influence path of major hazards, risk types and risk descriptions are identified through the compilation of various data, such as historical events as well as domestic and international issues and trends.

・Risk Measurement Assessment: Risk assessment models are introduced for scenario analysis to complete the quantitative assessment of the impact that risks have on business as well as potential opportunities.

・Risk Strategy: Based on the quantitative assessment results and the organization's current situation, adopt strategies for mitigation, transfer, acceptance, or control of climate risks and establish action plans for mitigation and adaptation.

・Objective Setting: Concrete organizational goals and indexes are established based on the outcome of risk strategy formulation. These goals are in turn allocated to business management units.

・Objective Monitoring: Organizational risks and opportunities are monitored regularly to ensure that milestones are met in time. An independent Risk Management Committee has been set up to effectively integrate the reviewing, monitoring, reporting and coordinated operation of the risk management matters of the entire Group.

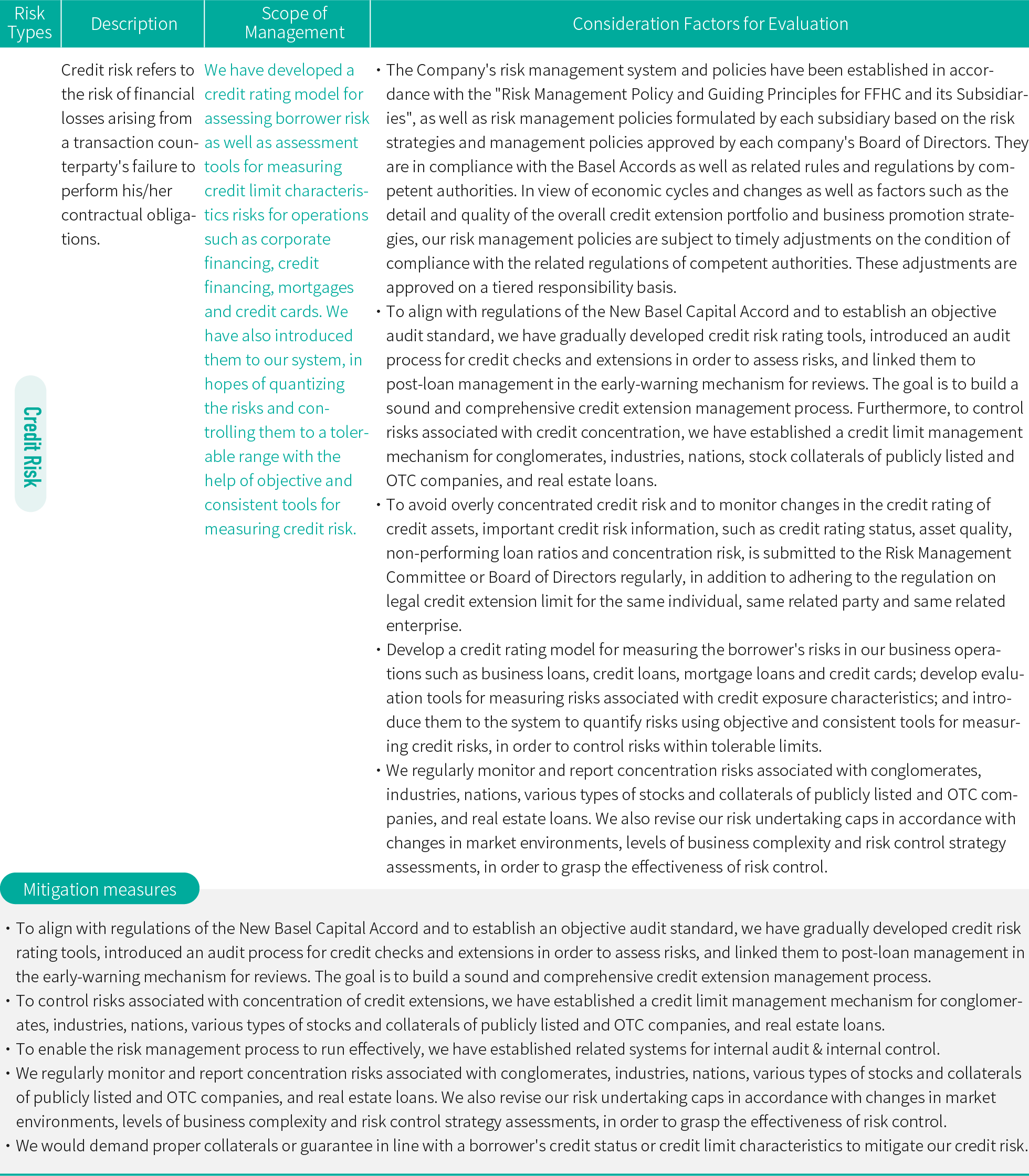

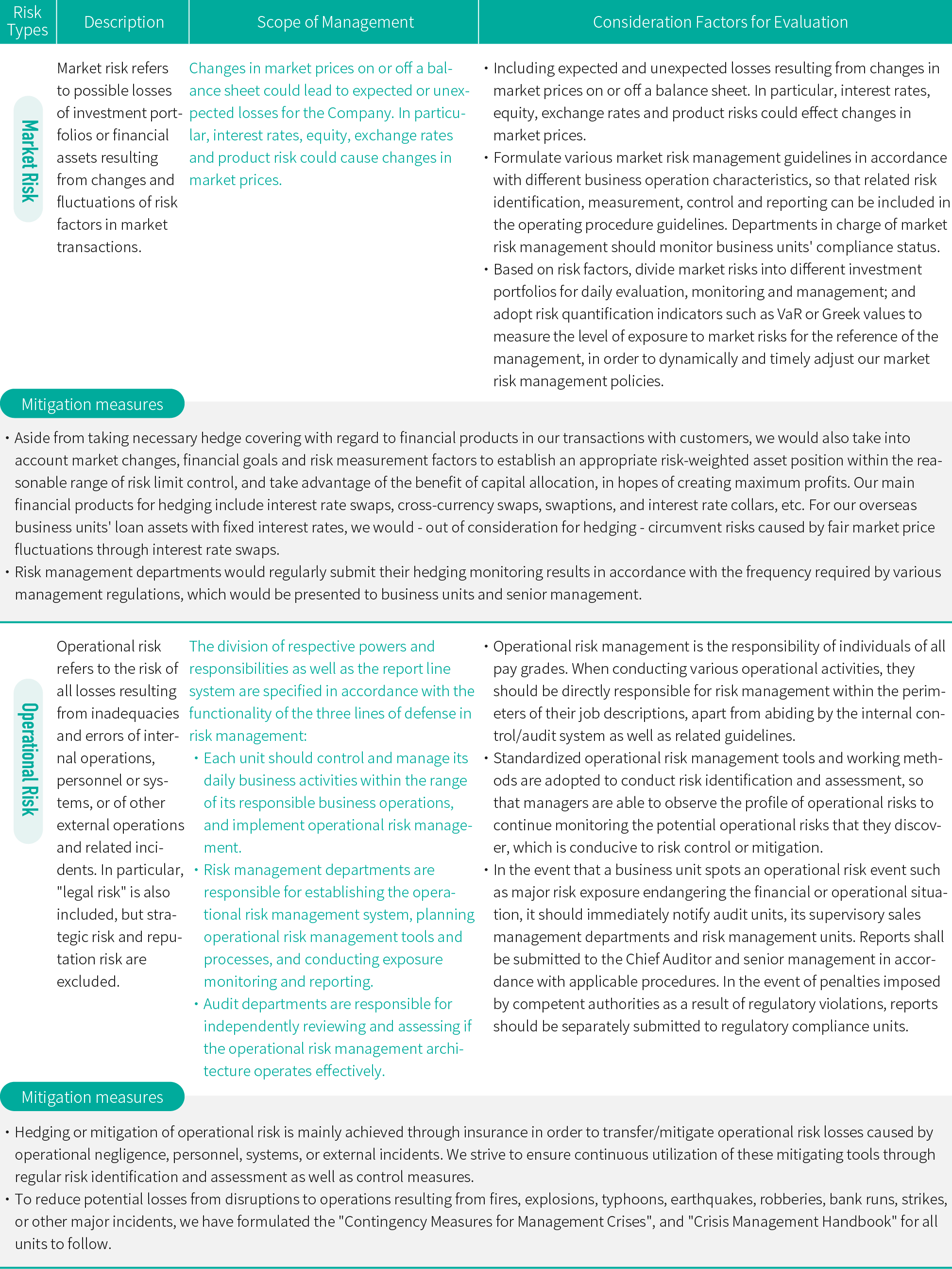

The Company has imposed caps on the maximum risk undertaking for the Group's and its subsidiaries' credit extensions and investment operations in order to control the Group's large risk exposures; The subsidiaries have set their respective capital adequacy ratio (CAR) alarm levels for various industries in order to maintain the Group's CAR; The Group regularly reviews its subsidiaries' main risk monitoring indexes, including credit risk, market risk, interest risk, liquidity risk, insurance risk, operational risk and emerging risk, in order to faithfully implement the early-warning and stop loss mechanisms; Effective internal control systems are implemented to reduce possible losses caused by risks.

Each subsidiary company would formulate its own control & management procedures for credit risk, market risk, interest rate risk, liquidity risk, insurance risk, operational risk and emerging risk, based on the characteristics of its business operations, including establishing and implementing the power delegation mechanism, quota management, monitoring indicators and reporting procedures, etc. The functionality of risk management is implemented through monitoring indicators as well as regular self-evaluations. Additionally, audit units would regularly check and verify the implementation status of risk management to ensure that the risk management mechanism is operating effectively.

As the types of global emerging risk items and related incidence gradually rise, the Company has also separately formulated the "Emerging Risk Management Guidelines" so that the Group can enhance corporate governance and administer assessments of emerging risks (such as trade war, global epidemic diseases, climate emergencies, information security risk, etc). By doing so, we have established a Group-level management mechanism for emerging risk items. The Company also adds or amends various risk management regulations and monitoring indicators in accordance with regulatory requirements or changes in the economic environment. In 2024, we additionally formulated the "Directions for First Financial Group's Management of Climate Change Risks", and amended related regulations such as the "Directions for FFHC's filing for Article 46 of the Financial Holding Company Act", "Regulations Governing FFHC's and Subsidiary Companies' Credit Extension to and Transactions with Stakeholders", and "Table of Maximum Risk Undertaking for Subsidiary's Credit Extension to/Investment in Same Individual, Same Related Party, or Corporate Credit Extension to the Same Conglomerate".

B. Risk Appetite

After taking business plans and risk profiles into account, we would set our risk appetite in accordance with the amount and level of risks we are willing and able to accept or assume. Aside from referencing reliable risk quantitative data, we would also incorporate past experiences and decision makers' macro vision. The Group's risk appetite is presented in two ways. The first is its CAR target, and the other one is risk limits (including credit risk, market risk and operational risk).

C. Analysis of Sensitive Scenarios & Stress Test

・The Group's sensitivity analysis includes interest rate risk, foreign exchange risk, and equity securities risk.

・The Group's subsidiary bank is one of the competent authority's domestic systematically important banks (D-SIB), which should be subject to a two-year stress test. It should also calculate various kinds of capital adequacy ratios and various profit and loss situations under severe recession scenarios in accordance with the Financial Supervisory Commission's "Operating Plan for Conducting Stress Tests on Domestic Banks" methodology.

D. Independent External Audits

First Financial Holding is subject to a full-scope examination by the Financial Examination Bureau, FSC once every two years, in addition to unscheduled targeted examinations. In particular, as the subsidiary bank has been designated as a domestic systematically important bank (D-SIB), it is required to file its CAR assessment results to the competent authority regularly. The competent authority also has more stringent demands with respect to the Bank's risk management process.

03. Risk management enhancement measures

A. System upgrade -

In response to the fact that the subsidiary bank has completed revision of its "Default Probabilities of Various Risk Grades in Corporate Finance", we have revised and added "Overdue Grades (W1 and W2), measurement methods and risk characteristics. The "Operation Directions for Credit Rating in Corporate Banking" and "Operation Directions for Grading in Specialty Financing" have also been amended accordingly.

B. Main risks -

credit risks, market risks, interest rate risks, liquidity risks, insurance risks, operational risks, and emerging risks.

・We amended the "Operation Directions for Bad Debt Provision in Domestic Business Units' Performance Reviews", and updated the "Product Median Reserve Ratio", in order to strike a balance between business expansion and risk pricing.

・The risk coefficient table has been corrected in order to stay in touch with the latest market changes and to increase effectiveness for measuring potential future exposure of derivative product transactions.

・To avoid omitting or failing to inspect the actual stakeholder's data and simplifying manual maintenance operation when conducting transactions beyond credit extension, we have linked up with data from the human resource information system (HRIS) for automatic investigation into related operations regularly. Reports are automatically produced for reference.

・Promulgated the amended "Illustrations on Banks' Regulatory Capital and Calculation Method of Risk-Weighted Assets and Tables" (BASEL III), and related regulations on capital accrual using standardized approaches for credit risk, in order to facilitate risk management and compliance.

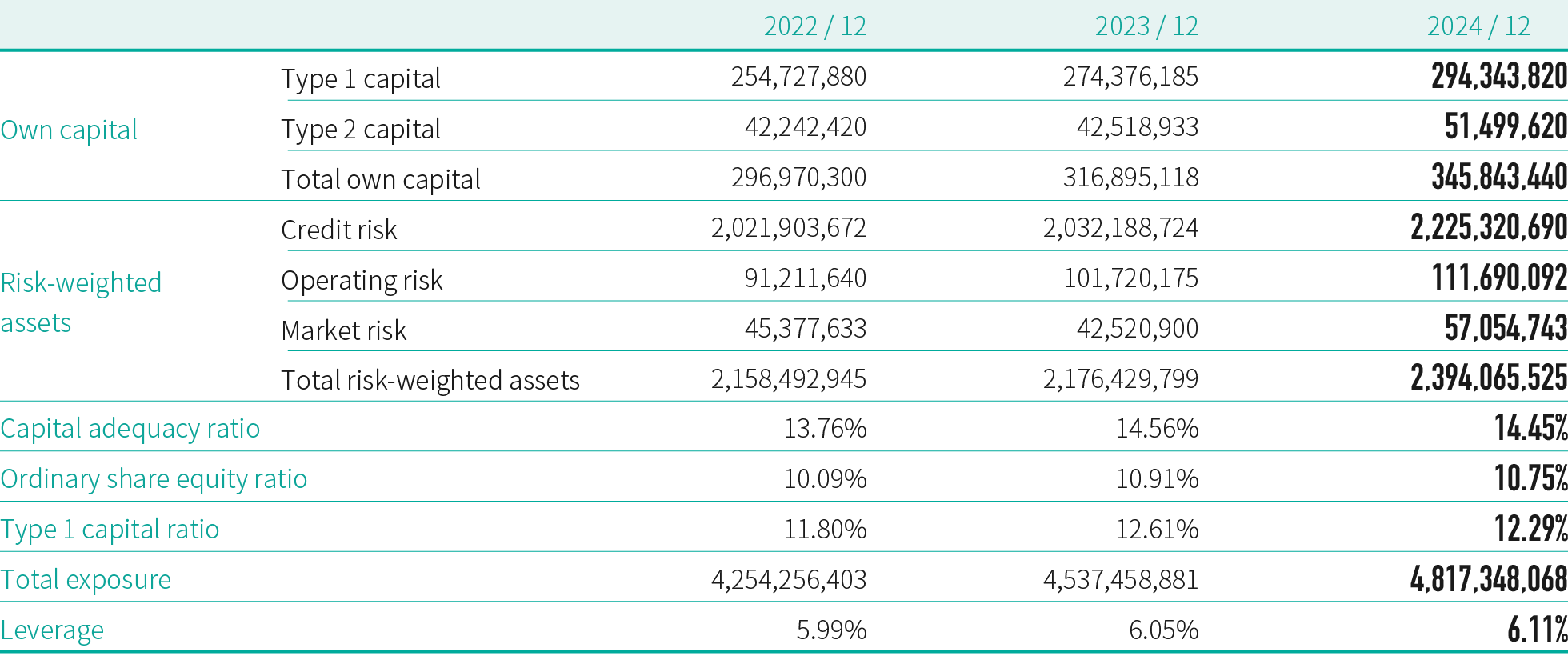

◎ Subsidiary First Bank capital adequacy ratioUnit: NT$1,000

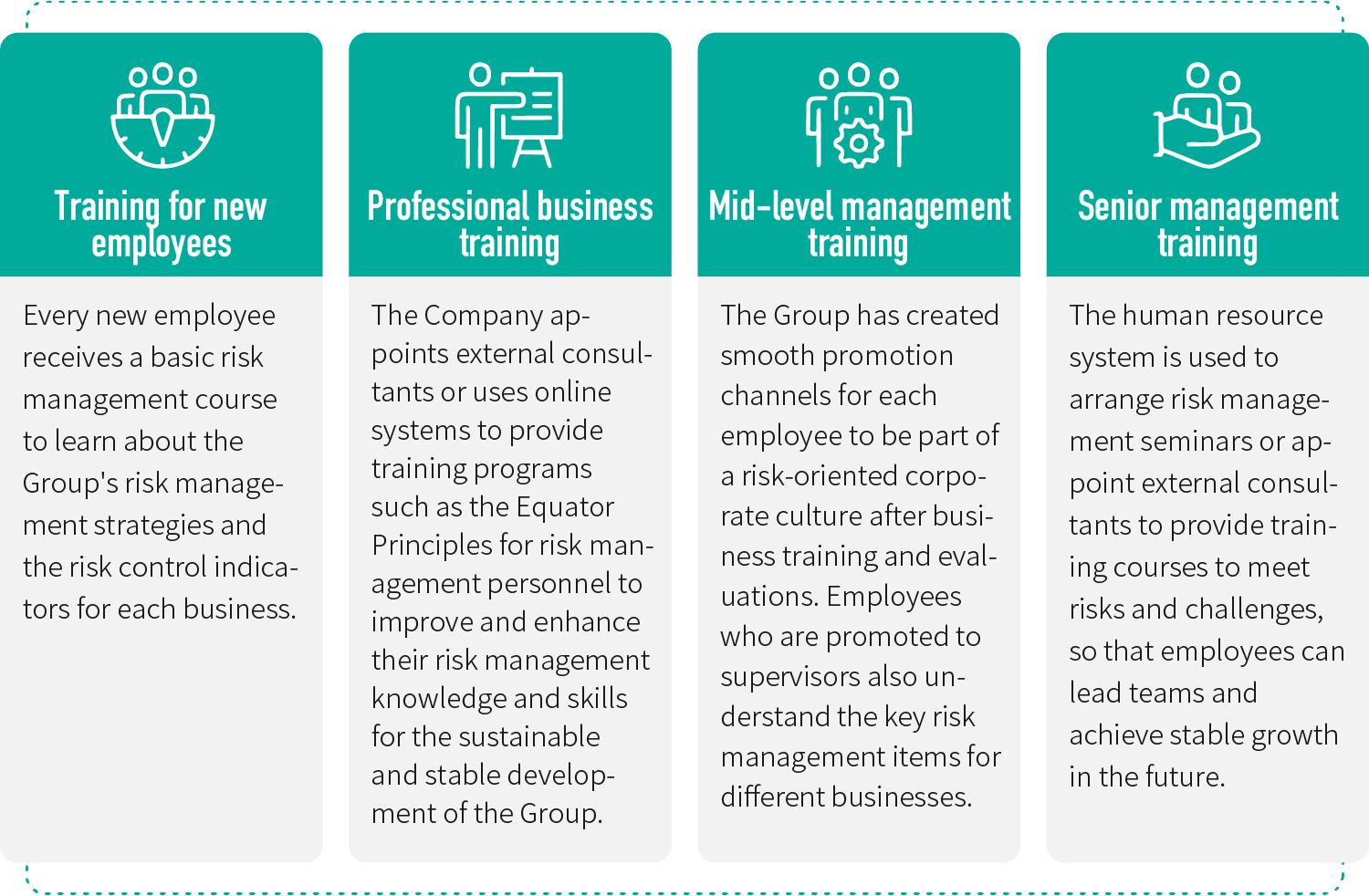

04. Establishment of the Corporate Risk Culture

To enhance and ensure smooth operation of the Group's risk management mechanism and to establish a risk-oriented corporate culture, we would invite and round up various companies within the Group to discuss current financial events and related changes, evaluate and adjust various risk control indexes and frequencies, and host risk management seminars from time to time. In the meantime, we also leverage the complementary online e-Academy to help build a systemic risk awareness. We hope that each and every Group employee understands FFHC's risk culture and core ideas, and we also conduct related educational training in risk management for promoted employees on various levels. In 2024, a total of 1,190 employees completed 32.6 hours of in-person or online educational training in courses or tests relating to risk management. For those who had failed to pass the tests, we also conducted retraining and retesting until the pass rate reached 100%.

Additionally, as the formats of financial products and services have become increasingly diverse and complicated, transaction disputes and financial crimes are more likely to occur as a result. To help our employees fully understand related domestic and international regulations and avoid regulatory gaps, we conducted three hours of training titled "Corporate Governance Forum-Money Laundering Risks Associated with Emerging Technologies" in 2024. A total of 49 Group Directors and Supervisors attended the training.

Establishment of Risk Management Culture Measures

◎ Connection between Risks and Performance

・Risk indicators (includes asset quality, customer complaints, regulatory compliance, and major incidents of internal control) are included in the standards for the distribution of performance bonuses for the President, senior management, and employees, and they affect the amount of the annual performance bonus.

・The performance evaluation items of the risk management unit include risk management indicators such as the capital adequacy ratio and leverage ratio, return on capital, and non-performing loan ratio control target achievement rates, employee training, and innovative measures. The evaluation results shall be used as an important reference for determining the performance bonus for the evaluated department.

・Performance Assessment:

A. With regard to the internal control and management checklist item of "points deduction standard for administrative efficiency" under "management performance" in the performance assessment, if an employee violates regulations relating to credit rating adjustments for corporate banking, and has been notified of three or more incidents of inadequacy by the Risk Management Department or fails to improve within the required timeframe after being notified during the assessment period, he or she shall be subject to points deduction in commensurate with the severity of negligence.

B. With regard to the "monitoring and management measures for controlling real estate credit concentration", an important management index relating to "profitability" and "management performance" in the "financial performance" of the performance assessment, we have also formulated related incentive measures.

C. "Capital utilization effectiveness" and the achievement rate of "economic profits" after taking capital cost into account have been incorporated in the performance assessment. We also conduct assessment contests for return on capital, including return on capital for net profit before withdrawals or deposits, the amount of increase in return on capital for gross operating profit before withdrawals or deposits, and the amount of increase in capital deduction, which serve as items worthy of extra points in the performance assessment of business units; Additionally, we would also conduct incentive activities to grade each unit's return on risk-weighted assets and average risk weights. Commendations/bonuses are awarded to outstanding units based on their scores.

•We continue to follow up on review opinions of internal audit units, accountants, and business administration units or deficiencies proposed by internal audit units, and matters requiring improvement listed in the internal control system statement. Improvements are submitted in writing to the Board of Directors and Audit Committee and used as an important item for penalties and rewards and performance evaluations of related units.

•The results of the compliance evaluation of the departments and subsidiaries are used as the basis for personnel evaluations.

◎ Risk Reporting measures

・We strive to establish a risk reporting mechanism for internal staff through related regulations, such as the Rules for the Regulatory Compliance System, FFHC's Guidelines for Reporting Regulatory Compliance Cases, Implementation Rules for the Internal Audit System, FFHC Incident Reporting Guidelines, Operational Risk Management Guidelines, and Credit Risk Management Guidelines.

・A range of transparent, equal and convenient complaints channels have been established including the "Supervisor Mailbox", "President's Mailbox", "Chief Auditor's Mailbox", "Ideas Mailbox", "Employee Support Hotline", "CEO Weekly", and "Good Articles" as well as public forums on the company intranet to ensure complaints are handled properly.

◎ Enhancement of the Risk Culture

・The Company organizes risk management seminars from time to time and invites subsidiaries to discuss recent changes in the finance industry to evaluate and adjust the risk monitoring indicators and frequency.

・We established the employee proposal system to encourage employees to actively identify and report potential risks.

・We publish the risk management newsletter each month and use the "Risk Management Report", "Special Report", and "Risk Management Terminology" to enhance the risk awareness of all employees and increase their professional knowledge and skills.

・Organize relevant education and training for emerging risks (such as information security risks, climate change risks and personal information protection risks) to improve risk resilience.

・Based on the "Standard Operating Procedures for New Types of Products", various business management units would discuss the profiles, operating procedures and internal control mechanisms of new types of products. Their proposals are submitted to the Business Decisions Committee or (Managing) Board of Directors for review; Before a new type of product is officially launched/goes online, it is necessary to conduct risk identification and assessment in accordance with related RCSA procedures and methods in the "Guidelines for Operational Risk Management Tools".

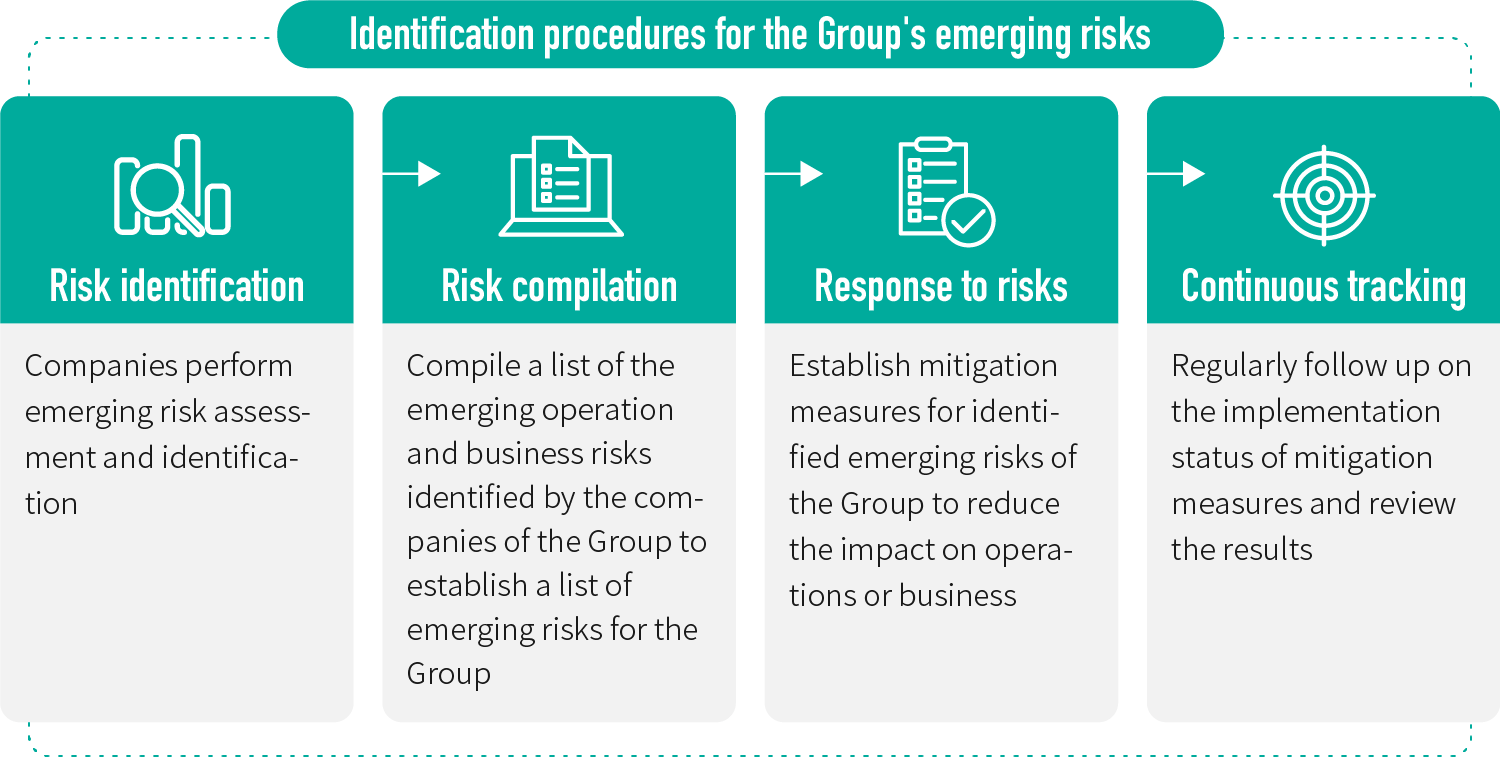

05.Emerging risks

The identification outcome of the Group's emerging risk includes "misinformation and disinformation created by AI" and "geoeconomic conflicts". The mitigation measures we have adopted to deal with the potential impact from such risks are indicated in the following table:

Risk Description - Misinformation and Disinformation Created by AI

Digital networks and social media have been inundated with large amounts of misinformation and disinformation over recent years. With the rapid development of generative AI (referred to as GenAI hereafter), financial institutions have also gradually adopted it. Even though GenAI helps improve operational efficiency while providing diverse services, it is likely to entail personal data leaks, information security issues, and related legal risks. In addition, people may have concerns about truthfulness of the generated content, or whether information is made up. Some crime syndicates even use GenAI to impersonate as financial institutions to conduct fraud, undermining society's trust in the financial system while impacting financial institutions' risk management and reputation.

Potential Impact

・Investment Risk: Investors and traders overreact due to misinformation or disinformation, which increases market fluctuations while impacting investment portfolios and trading performance.

・Operational Risk: Misinformation could also cause the management team to make wrong judgment calls in management policymaking, which would lead to failure, unnecessary cost burdens, and operating losses.

・Information Security Risk: In case information security management is less than perfect, customers' personal data and companies' trade secrets are prone to leaks, or misinformation may be disseminated.

・Property Damage Risk: Impersonating as the Company, a scam syndicate could claim that "the customer has been impersonated to apply for a loan or open an account", and use it as an excuse to contact the said customer, claiming that it has already helped notify the police to ensure the safety of customer property. Afterwards, the syndicate would arrange a phony policeman to call the customer, trying to extract personal data under the guise of police investigation and causing property damage to the customer.

・Compliance Risk: To address risks associated with use of misinformation and disinformation derived from GenAI, governments of various countries will progressively introduce new legislation or amend existing regulations. The companies under the Group need to adjust their internal guidelines in response to regulatory amendments in a timely fashion. They also need to enhance employees' ability to identify GenAI-related risks and contingency countermeasures.

Mitigation Measures

Short-term:

・Disseminate the correct message to investors and customers via various channels, including bank statements, and transaction app push; provide anti-fraud information to customers regularly; set up a dedicated counter-fraud zone on the official website; make a list of frequently seen investment fraud patterns and related information from government agencies and continue to update it; and raise the anti-fraud awareness on the official social media platforms.

・Clearly remind customers to call the "165" anti-fraud hotline for verification and reporting when they suspect an impostor of posing as a Company employee, or find a counterfeit and phony official website, marketing advertisement, or an impostor using apps to misguide or scam people.

・Install an instantaneous and smooth channel for the distribution of material messages and communications about customer complaints; make timely clarifications to block and eliminate misinformation; and prevent negative public sentiments from spreading, so that society's impressions on the Company are not impacted.

・Increase employees' information security awareness of fraud patterns derived from emerging technologies through regular educational training and bulletin reminders.

Additionally, the following medium- and long-term mitigation measures are also adopted:

・Use big data and AI technology to conduct real-time monitoring and identification of misinformation and disinformation, in order to facilitate correct decisions.

・Build a robust risk management system through AI technology and joint data defense; enhance cooperation with the tech sector to create a more sturdy anti-scam ecosphere.

・Actively set up a channel for monitoring and verifying disinformation as well as instant notification with third parties or government agencies to jointly maintain financial market stability.

・Continue to follow up on the latest relevant regulatory developments and updates or supervisory trends, and use them as foundation to distribute regulatory reports or education training materials, so that various units can stay on top of relevant regulatory messages in a timely manner. Internal guidelines are also adjusted accordingly, and scenario tests are conducted in line with demands of competent authorities. We would also evaluate to set up an emergency response team to counter cases involving impostors and cope with various patterns of impostor incidents.

Risk Description - Geoeconomic Conflicts

Whether it's Brexit, China's emphasis on self-sufficiency through internal demand and circulation, or Trump's tariff and trade war, they all represent the emergence of global protectionism, isolationism and deglobalization, as nations weaponize economy and limit products, knowledge, services or technology, in order to gain geopolitical advantages and solidify their sphere of influence. Therefore, enterprises and governments need to strengthen supply chain resilience and divert market risks, in an attempt to address uncertainties associated with geoeconomic risks.

Potential Impact

・Default Risk: Geoeconomic competition may lead to import/export restrictions and tariff barriers, which impact corporate profitability. Economic sanction and trade war are also likely to ramp up raw material prices. As capital expenditures increase, solvency is adversely affected, and the risk of default on financial institutions' loans goes up.

・Credit Risk: Due to fear of geoeconomic conflicts, borrowers' operations may be impacted by trade risks such as trade deficit and weak foreign exchange rates, which further increases credit risks for financial institutions.

・Systemic Risk: As price fluctuations in the global energy, raw materials and financial markets exacerbate, investment gains are feared to decline. Market hedging sentiment would rise, and investors scramble to dump financial products in their possession, triggering a price collapse while intensifying financial market fluctuations.

・Rising Corporate Costs: Rising tariffs would lead to an increase in the prices of imported products, which represents a severe blow to import-oriented companies. This would invariably jack up operating costs for companies and impact their bottom line.

・Compliance Risk: People fear that economic sanctions and technological blockades may increase compliance and operational risks for financial institutions.

Mitigation Measures

Short-term:

・Pay attention to international political and economic messages, various countries' economic indicators, changes in their overall status, and rating reports; monitor losses/gains and changes in our investment positions, asset quality, and credit risk concentration regularly; keep a tight leash on related exposed positions; adjust our investment strategies discreetly, and issue timely warnings or put forth countermeasures in response to material events.

・Develop new clientele actively; divert business operations; reduce reliance on one single country or supplier; and adjust risk quotas of various countries, depending on the situation.

・Support the government's push for the Six Core Strategic Industries, including information and digital technology, cybersecurity, medical technology and precision health, green and renewable energy, national defense and strategic industries, and strategic stockpile industries, so that we can stay on top of business opportunities associated with reset global supply chains.

・Continue to understand our borrowers' operating status through post-loan reviews and early warning operations; and adopt action plans or debt collection programs before credit default in order to maintain the quality of our credit assets.

・Collect the latest relevant regulations of various countries and formulate corresponding internal guidelines for compliance by our business units.

Additionally, the following medium- and long-term mitigation measures are also adopted:

・Beef up cooperation with international financial institutions to build up a risk-sharing mechanism, in an effort to reduce impact of geoeconomic conflicts.

・Manage our credit exposure discreetly; and avoid concentrating credit positions on a specific region to reduce the impact of unfavorable factors on our credit operation.

・Utilize fintech to streamline manual operations and reduce operating costs; and increase transaction monitoring capabilities to avoid the risk of being sanctioned.

・Continue to remind managers to be closely mindful of international political and economic situations; refine our pre-loan credit investigation capabilities; urge colleagues to enhance crisis identification; pay attention to borrowers' operating status; and be mindful of diverting concentration on one particular industry or customer.

Third line model - Independent internal audit unit

The Company and its subsidiary bank, securities company, securities investment trust company and insurance company have all set up internal audit units that report to the Board of Directors. A general audit system has also been established, which audits and assesses the internal control system designed and executed using the first and second models as well as the effectiveness of the risk management system, based on an independent and non-partial spirit. It also offers timely improvement suggestions to reasonably ensure that the internal control system can continue to be effectively enforced. The suggestions also serve as a basis for reviewing and amending the internal control system. Furthermore, the internal audit units would continue to follow up on and re-examine review comments as well as audit faults identified by financial examination agencies and accountants, those submitted by themselves and business units, as well as items marked for further improvement in the internal control system declaration. The status of their follow-up audits and improvement, regularly submitted to the Board of Directors and Audit Committee in writing, serves as an important index for awarding or punishing related departments as well as performance assessments. The goal is to maintain the operation of an effective and appropriate internal control system.

To enhance the functionality of the second and third models such as regulatory compliance and internal audit and control, the Company would ask its various departments and subsidiary companies to be mindful, and review the completeness and effectiveness of related internal control regulations and control measures in its "Review Seminar for Improving Internal Control System Faults & Regulatory Compliance". The meeting focuses on the emphasis of financial examination noted by the Financial Supervisory Commission and the financial holding company's internal audit seminar, the annual examination emphasis announced by the Financial Examination Bureau, main faults identified in examinations of the financial industry, as well as the recent peers' fault patterns in penalty cases. The Company would ask various audit units to incorporate the aforementioned items in their annual audit focus, in order to implement the three models of internal control and facilitate sound management for the Company. To implement performance assessments, we would annually assess the results of related audit operations, including the subsidiaries' internal audit units and systems as well as their verification for internal audit and audit management, in accordance with the Company's assessment regulations governing the evaluation of subsidiary companies' audit operations. The results would be presented to the Board of Directors of each subsidiary as an important basis for the performance assessment of each audit unit.

With regard to the execution of the Company's 2024 internal audit operations and formulation of our 2025 audit plan, we would adopt a risk-weighted management approach, in addition to referencing the latest changes in regulations, the competent authority's updated examination focus, ratings for the internal control execution of various units (including subsidiaries), and the business characteristics of various units (including subsidiaries). In addition, the two models would supervise the examination outcome from the internal control system itself. After being reviewed by the audit units, the outcome, along with internal control faults and the improvement status of anomalies as identified by the audit units, would be used for evaluating the effectiveness of our overall internal control system. By doing so, we hope to consummate self-evaluation in the Group's internal control system. Additionally, subsidiary First Bank has implemented a risk-oriented internal audit system by establishing a series of risk-oriented methods and procedures to evaluate internal audits. This acts as a foundation for compiling audit plans to determine the frequency of internal audits based on the assessed risk level, thereby deploying audit resources with more effectiveness as well as reinforcing audit focus on critical risks.

◎ Key audit criteria

・The status of implementing measures to prevent money laundering, combat terrorism financing, and counter weapon proliferation.

・The status of enforcing of the regulatory compliance system.

・Supervision and management of the reinvestment businesses.

・The status of implementing and operating the corporate governance system.

・The Group's risk management and control mechanism.

・Conduct information security management, and supervise & guide subsidiaries' implementation on updating relevant plans and operations of the information system, information security defense, early warning monitoring, and the contingency response drill mechanism.

・Personal information protection.

・The status of executing the whistle-blowing system, including educational training.

・The status of declarations in compliance with the Financial Holding Company Act.

・The status on implementing control procedures and the sampling/verification mechanism to guard against conflict of interest regarding domestic equity investments or inappropriate transactions.

・The status of audits and management initiated by the internal control system.

・The status of driving ESG in sustainable finance and implementation of IFRS svstainable imformation disclosure standards.

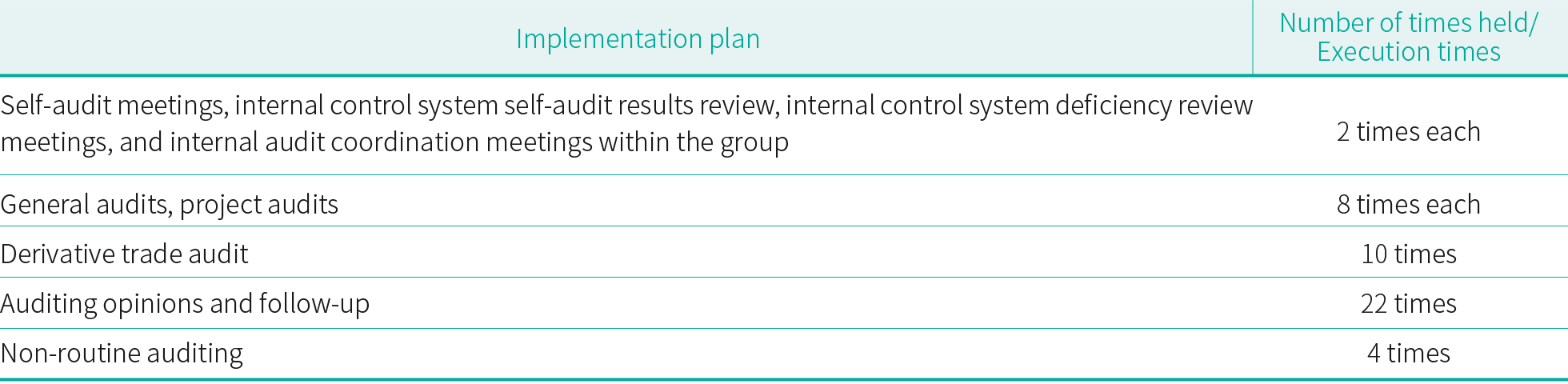

◎ Implementation of the internal audit system in 2024 is as follows

Business Continuity Management Mechanism

In order to quickly pass the information on incidents and to grasp the timeliness of processing, the Company and its subsidiaries shall, when incidents occur, divide incidents into major incidents and general incidents according to the "FFHC Incident Reporting Guidelines", and according to the degrees of impact, divide them into three levels: A, B, and C and handle them in accordance with the "Incident Handling Notification Procedures", and follow the principles of notification, handling, follow-up, etc. prudently, so to effectively prevent the expansion of disasters and reduce the impact.

In addition, to promptly and effectively handle the business crisis of the Company and its subsidiaries (including the occurrence of bank run, robbery, theft, major malpractice, financial crisis, major investment failure, information crisis (including: data leakage, system interruption, etc.), fire, explosions, natural disasters, customer collective petitions and other major events or disasters), hoping to quickly pacify the incident or restore operations, and reduce the harm, the Company has formulated the "Crisis Response Principles for the Company and its Subsidiaries". When a crisis occurs, the business responsible unit shall promptly deal with it, and in addition to taking general contingency measures for its related business, it shall also adopt different contingency measures for business crises caused by various reasons. The Company shall set up a crisis management team when necessary, and the risk management department shall be responsible for the establishment of case files, convening meetings, case listing and tracking records, and reporting the case and handling process to the Company's supervisors at all levels at any time, until the incident subsides and the crisis is lifted.

To ensure uninterrupted operation for the financial system, and to provide people with reassuring, convenient and diverse financial services as the basis of innovative FinTech developments, the Company and its subsidiary bank, securities company and life insurance company implement and execute measures for information security and privacy protection. Please refer to the "Information Security and Privacy Protection" chapter for more details on related planning and execution status.