Economic Factors >

Ethical Management and Fair Customer Treatment

Ethical Management and Fair Customer Treatment

Ethical corporate management execution status

The Company has formulated the "Ethical Corporate Management Best Practice Principles & Guidelines for Conduct", which serves as the policy for the companies and organizations within the Group to observe when it comes to ethical corporate management. These guidelines clearly stipulate a confidentiality mechanism, as well as preventive measures to prohibit, supervise and report unethical conduct such as corruption, bribery, monopoly, unfair competition, and inside trading. It is applicable to Group employees around the globe, subsidiaries, and contractors/suppliers/service providers. Enterprises and organizations within the Group are also required to combine the ethical management policy, employee performance evaluations, and human resource policy. Major violators of ethical conduct shall be punished in accordance with the relevant laws or human resource management rules. The violator's job title, name, date of violation, contents of violation, and handling shall be disclosed on the Company's internal websites, in order to establish a clear and effective discipline and grievance system. In addition, the Corporate Governance Group of the Administration Management Department has been put in charge of planning and managing affairs relating to ethical management. The "Ethical Management Committee", which reports to the Board of Directors, has been established as the dedicated entity for promoting ethical operations. Three independent directors are appointed as the committee's members responsible for formulating and revising the Group's ethical management policy. To achieve sound ethical management, the "Ethical Management Committee" shall provide the Board of Directors with a report on the Group's fulfillment and adopted measures about ethical operations once every six months, conduct regular analysis and assessment on the Group's risks from unethical conduct, formulate plans to prevent unethical conduct, and report the implementation status of internal/external education training on ethical operations and whistleblowing systems within the Company and all subsidiaries. It should also direct various subsidiaries to step up their anti-fraud promotions and internal whistleblowing systems, and enhance education training on personal data protection. With respect to implementation of ethical management, relevant organizations have studied, planned and put forth the following countermeasures:

Measures for implementing ethical management

Aside from establishing the "Rules for Implementing Accountability Systems for the High Asset Wealth Management Business"- which clearly defines the basis of accountability, applicable subjects, and procedures of the high asset wealth management business - the subsidiary First Bank has also set up a Board-level "Accountability Committee", which is in charge of accountability for the high asset wealth management business and is consistent with the Financial Supervisory Commission's requirements to strengthen the supervision, management and responsibility of such business operations. Furthermore, the "Guidelines for Implementing the Responsibility Map System" as well as the responsibility map (including the organizational chart for corporate governance, accountability assignment chart and diagram for internal reporting flow) were formulated in December 2024. The goal is to clearly delineate the scope of responsibility between the Chairman and senior management personnel, and to establish a responsibility-based accountability system, which could serve as foundation for implementing a corporate culture of ethical management and strengthening the corporate governance structure. To build a sound system for managing intellectual property, the Company has also formulated the "Intellectual Property Management Policy" and "Directions for Trade Secrets & Intellectual Property Management". Subsidiary First Bank received Taiwan Intellectual Property Management System (TIPS) verification for the third time on Oct. 24, 2024 (valid till Dec. 31, 2025), making it a bank that has simultaneously obtained TIPS verification (class A) for both patents and trademark.

Ethical corporate management education and training

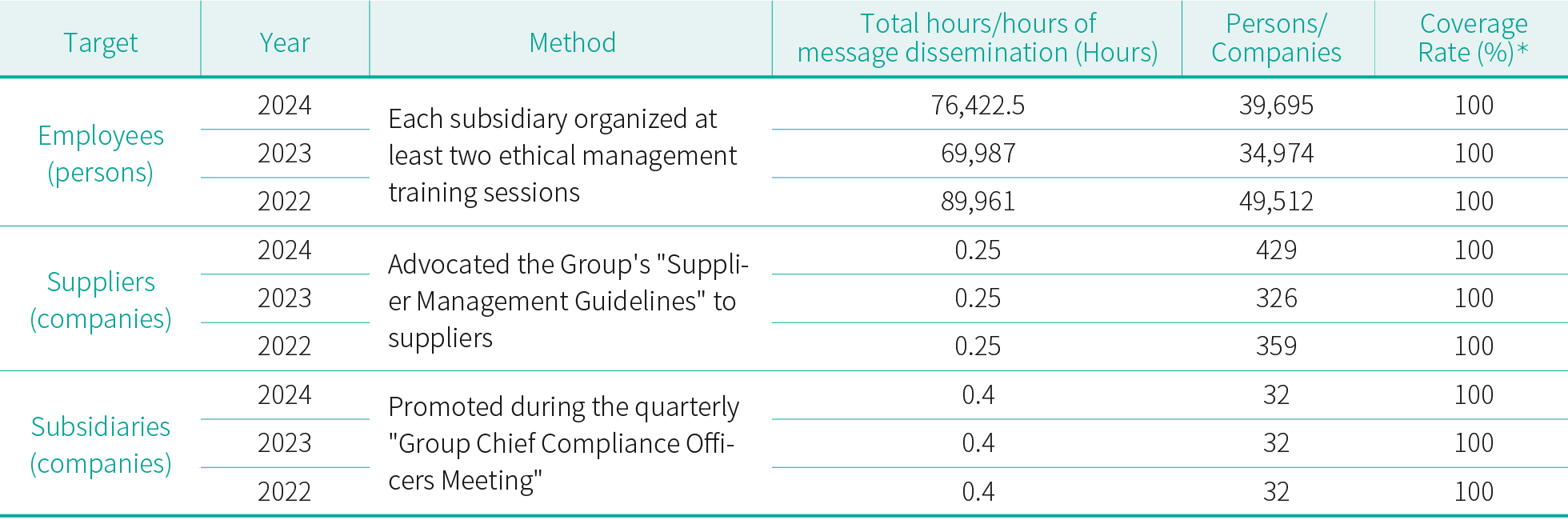

The Company conducts education on regulations related to integrity management of subsidiaries through the "Group Chief Compliance Officers Meeting" quarterly. We urge subsidiaries to organize education, training, and promotion events related to ethical management for employees, and to communicate the group's ethical management policy and whistleblower system. In 2024, the group provides all employees worldwide with a total of 76,422.5 hours of education and training for 39,695 participants. Counterparts that do business with the Company are invited to participate in the activities, so that they fully understand the Company's unethical conduct prevention plans and zero tolerance policy.

◎ Ethical Management Education and Training in the past three years

*:Coverage Rate= Required Participation (Persons/Companies)/Actual Participation (Persons/Companies)

In 2024, the FFHC had no financial losses resulting from litigation involving fraud, insider trading, antitrust, anti-competitive behavior, market manipulation, corruption, or other violations of financial industry laws and regulations.

Code of Conduct

The rate of the Group's Directors, Supervisors, managers and employees signing the "FFHC Code of Conduct for Directors, Supervisors, and Managers" and "FFHC Code of Conduct for Employees" note is 100%. Furthermore, the rate of employees hired by subsidiary First Commercial Bank in its overseas operating locations signing local language versions (English, Vietnamese and Khmer) of the "Code of Conduct for Directors, Supervisors, Managers, and Employees" is also 100%.

Subsidiary bank's control measures to guard against corruption and fraud committed by financial advisors

・To align with the "Principles of Internal Control Operations Relating to Banks' Efforts to Guard Against Embezzlement of Customers' Funds by Financial Advisors" example table amended and promulgated by the Bankers Association on July 26, 2021, and the newly added 21 "typologies of suspected embezzlement of customers' funds by financial advisors", including proxy operation on behalf of the customer, fund transfers, associated accounts and other behavior, the subsidiary bank has formulated the "Investigation Procedures for Abnormal Behavior or Transactions Involving First Commercial Bank's Financial Advisors and Management Directions for Supervision and Implementation", in order to strengthen its control mechanism targeting financial advisors' money management operations. An independent investigation team made up of Headquarters units or personnel that are independent from the financial advisor's business operations has also been set up to look into related abnormal behavior, as part of our efforts to implement regulatory compliance, consumer protection and risk management, as well as to demonstrate that we value ethical management and fair customer treatment.

・Additionally, to prevent financial advisors from misappropriating customers' funds, we have enhanced related internal control measures, including the implementation of standard operating procedures for financial advisors' customer visits, in an effort to strictly enforce independent front-end and back-end operations. All money management transactions are linked to bill deductions from our customers' accounts, without requiring them to separately present withdrawal certificates; Financial advisors are strictly prohibited from carrying out cash deposits or withdrawals throughout the entire process on behalf of their customers. Furthermore, the Bank, when necessary, would conduct spot checks to see if financial advisors have manifested abnormal behavior, such as retaining customers' passbooks, seals, or signed blank transaction documents, etc. The Bank would also designate dedicated personnel to check if there are any inappropriate fund exchanges between financial advisors and their customers during their designated leave days every year. The Bank also stipulates that a financial advisor's tenure with the same business unit shall not exceed six years, in addition to reinforcing the second-person service mechanism. Branch executives are also required to personally visit or call important money management customers in order to prevent malpractice resulting from these customers overtrusting their money management advisors.

・The Bank has also installed the "Management System for Abnormal Money Management Patterns". With this system, the Bank is able to identify and detect early warning signs through analyzing transaction behavior between the teller and the customer. This fully automatic monitoring and control system not only can shorten the monitoring cycle, but also can spot new corruption patterns instantaneously. Moreover, the Bank is able to swiftly analyze trends and anomalies through visualized forms such as charts and figures. This is conducive to instantaneous decision-making, enabling the Bank to boost the effectiveness of its controls over abnormal behavior.

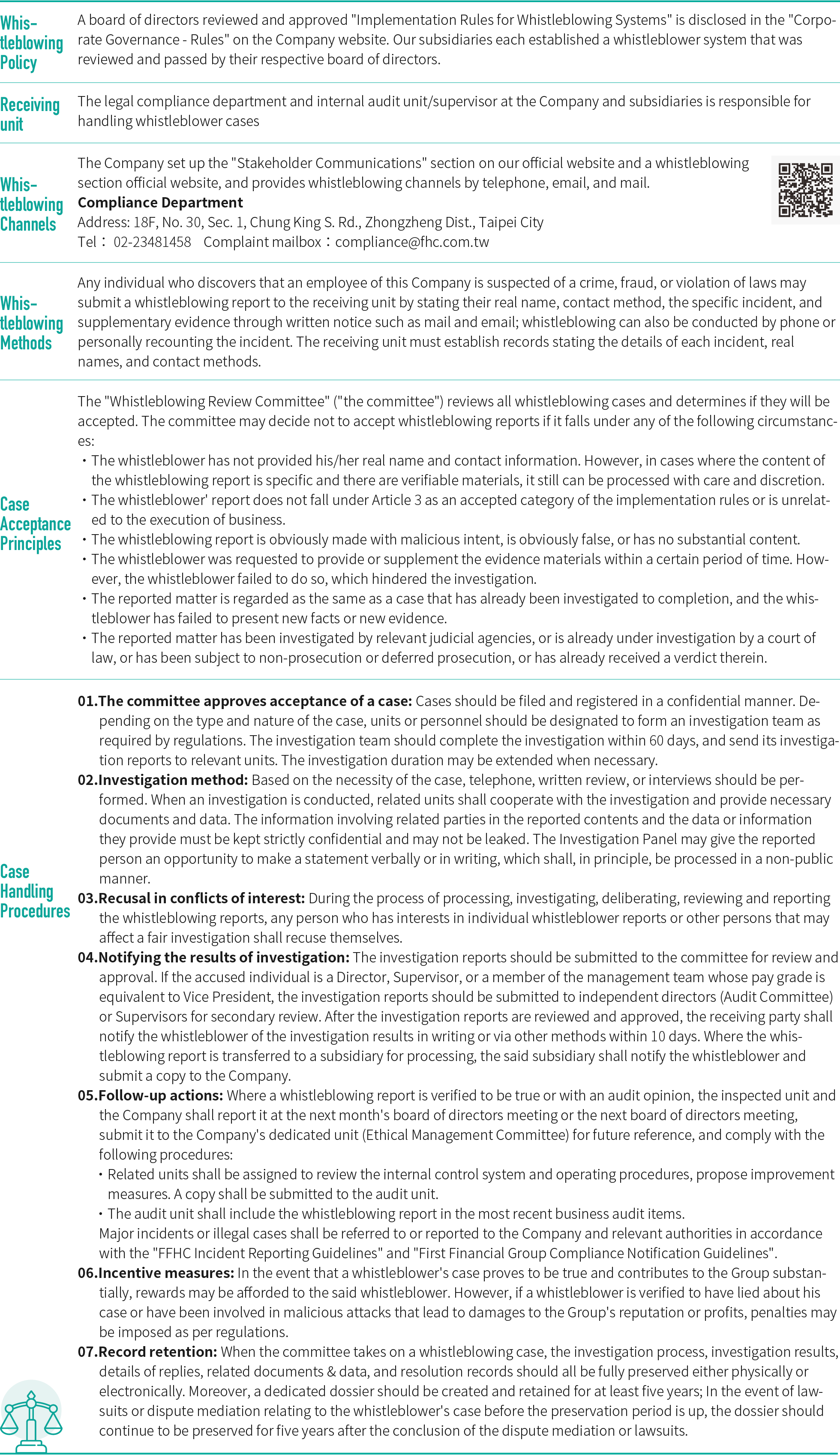

Whistleblower System, Process, and Results

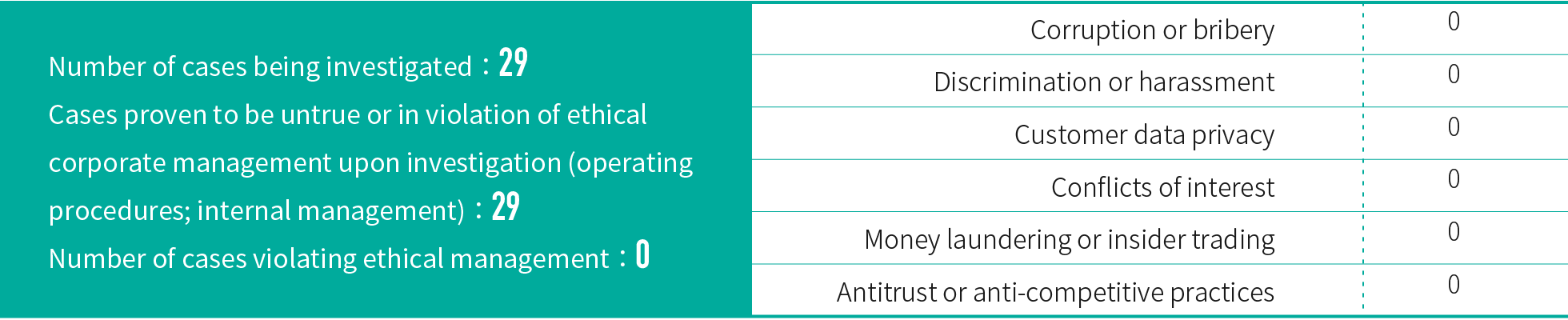

In 2024, the Group received a total of 52 whistleblower's cases. In particular, 23 cases were dismissed for lack of substantial facts or because they were unrelated to our business operations. For the remaining 29 cases, their case types, investigation results, reviews and remedy measures have all been submitted to the Board of Directors of respective companies, as well as the Company's Ethical Management Committee and Board of Directors for future reference. In 2024, the Group did not incur any financial losses due to corruption-related cases.

Implementation of Fair Customer Treatment

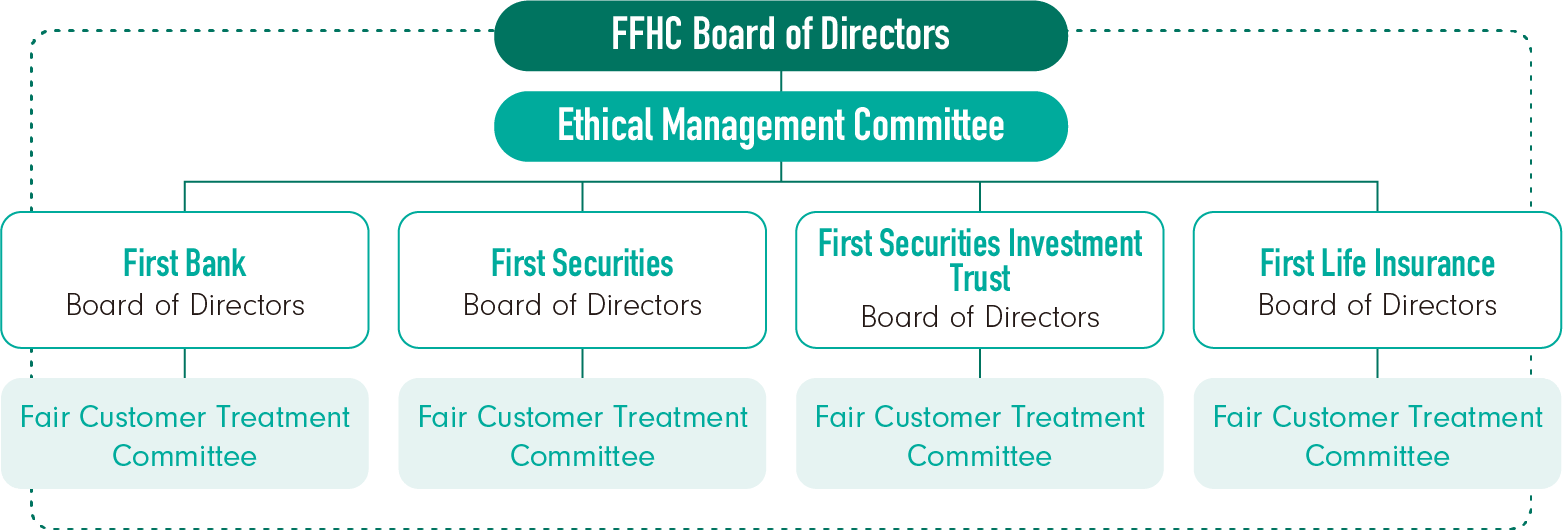

Ethical corporate management is the cornerstone of fair customer treatment in the financial industry. The Company has formulated the "Code of Conduct for Ethical Management" in accordance with the "Principles for Fair Treatment of Customers in the Financial Services Industry" and "Standards Governing Friendly Financial Service". It stipulates that, during the course of product/service R&D, provision or sales, companies within the Group shall not infringe upon the rights of consumers or any other stakeholders. It also demands that related operating procedures and code of conduct be formulated, and that education training be conducted. First Commercial Bank, First Securities, First Securities Investment Trust and First Insurance have all formulated and promulgated the "Policy of Fair Customer Treatment & Related Strategies", which have been submitted, reviewed and approved by the Board of Directors of each company. Furthermore, inspection comments made by internal audit divisions about improvement measures for inadequacies relating to consumer protection are regularly incorporated in the regulatory compliance status report, which is submitted to the Board every six months. First Bank has also formulated the "Handling Procedures for the Classification & Reporting of Customer Complaints", which requires immediate identification upon the receipt of a customer complaint case. It also calls for monitoring, investigating and analyzing the root cause of a customer complaint, in addition to creating a risk-oriented reporting mechanism. In 2024, the Bank was once again ranked in the top 25% in the Financial Supervisory Commission's review for fair customer treatment. First Life Insurance made the list of top 26%-50% companies. First Securities, a small- or medium-sized securities firm, is subject to review once every two years. In 2023, it was chosen as one of the top 26%-50% companies. Additionally, each company has also established its own dedicated committee responsible for supervising the advancement and implementation of "Fair Customer Treatment in the Financial Services Industry". These committees review the implementation status of fair customer treatment on a quarterly or semi-annual basis. They also put forth and submit remedy measures to the Board of Directors of their respective companies, before submitting them to the Company's Ethical Management Committee and Board of Directors. Related education training on "Fair Customer Treatment in the Financial Services Industry" was also conducted. A total of 7,759 individuals have undergone training, with a completion rate of 100%.

To better protect the rights of financially disadvantaged demographic groups such as elderly people and persons with disabilities, the Company partnered with the Economic Daily News in 2024 to jointly host the "Ethical Finance-Counter Fraud; Prevent Scams and Build a Safe Financial Environment" forum, where we took a deep dive into how to integrate resources and how to take advantage of AI technology to guard against financial crimes and protect consumers' properties and rights. With respect to improper marketing to disadvantaged people or customer complaints and disputes arising from rules violations, First Commercial Bank has incorporated them into the annual review of business units. They are also incorporated into the evaluation scope of the Compliance Risk Assessment (CRA) and Institutional Risk Assessment (IRA). The "Reference Practices for Bank Services for People with Dementia or People Suspected of Dementia" published by the Bankers Association has also been incorporated into the "Friendly Financial Service Guiding Handbook"; The Bank also compiled personality trait analysis reports on vulnerable demographic groups (including the elderly) published by the Financial Conduct Authority (FCA) in the UK, which have been shared with our front-line staff at operating locations for reference; 24 red-flag indicators for elder financial exploitation published by FinCEN in the U.S. have been introduced and applied to over-the-counter outreach operations at our branch offices; The Bank referenced the "Recovering from Elder Financial Exploitation" report promulgated by the United States Consumer Financial Protection Bureau as well as domestic practices to formulate the "Standard Protocols for Assisting Elder Customers in Retrieving Funds Lost to Financial Exploitation", and compiled measures to protect vulnerable people from financial exploitation, such as FinCEN's Elder Financial Exploitation: Threat Pattern & Trend Information report, in an effort to better protect the rights of such demographic groups; Furthermore, the Bank also compiled emerging measures for the economic inclusion of persons with disabilities that were promulgated by the International Finance Corporation (IFC), the Japanese Financial Services Agency's directives for eliminating discriminations against persons with disabilities, and the United States Consumer Financial Protection Bureau's (CFDB) penalty cases pertaining to discriminatory home mortgage applications, which have been provided to various units for education training and promotion. In addition, the Bank also follows up on the implementation status of service measures for the fair treatment of elderly customers on a quarterly basis, which is submitted to the Committee for Advancing Fair Customer Treatment.

To protect consumer rights, First Bank, First Securities, First Securities Investment Trust and First Life Insurance have all implemented the Know Your Product/Service (KYP) policy. Since Q1 of 2016, First Bank has completely suspended the undertaking of complex and high-risk products. With respect to structured notes, the Bank has formulated special notifications to customers in addition to informing them of the risks associated with structured notes, in order to make sure that customers are well aware of our product details. In 2024, the Group recorded six incidents relating to product sales and services, for which we were subject to regulatory punishments and underwent litigation proceedings. The total loss was NT$600,000 (please refer to the appendix: sustainable operation indicators). The Group has remedied the relevant deficiencies and added relevant control mechanisms, effectively enhancing the protection of consumers' rights and interests.

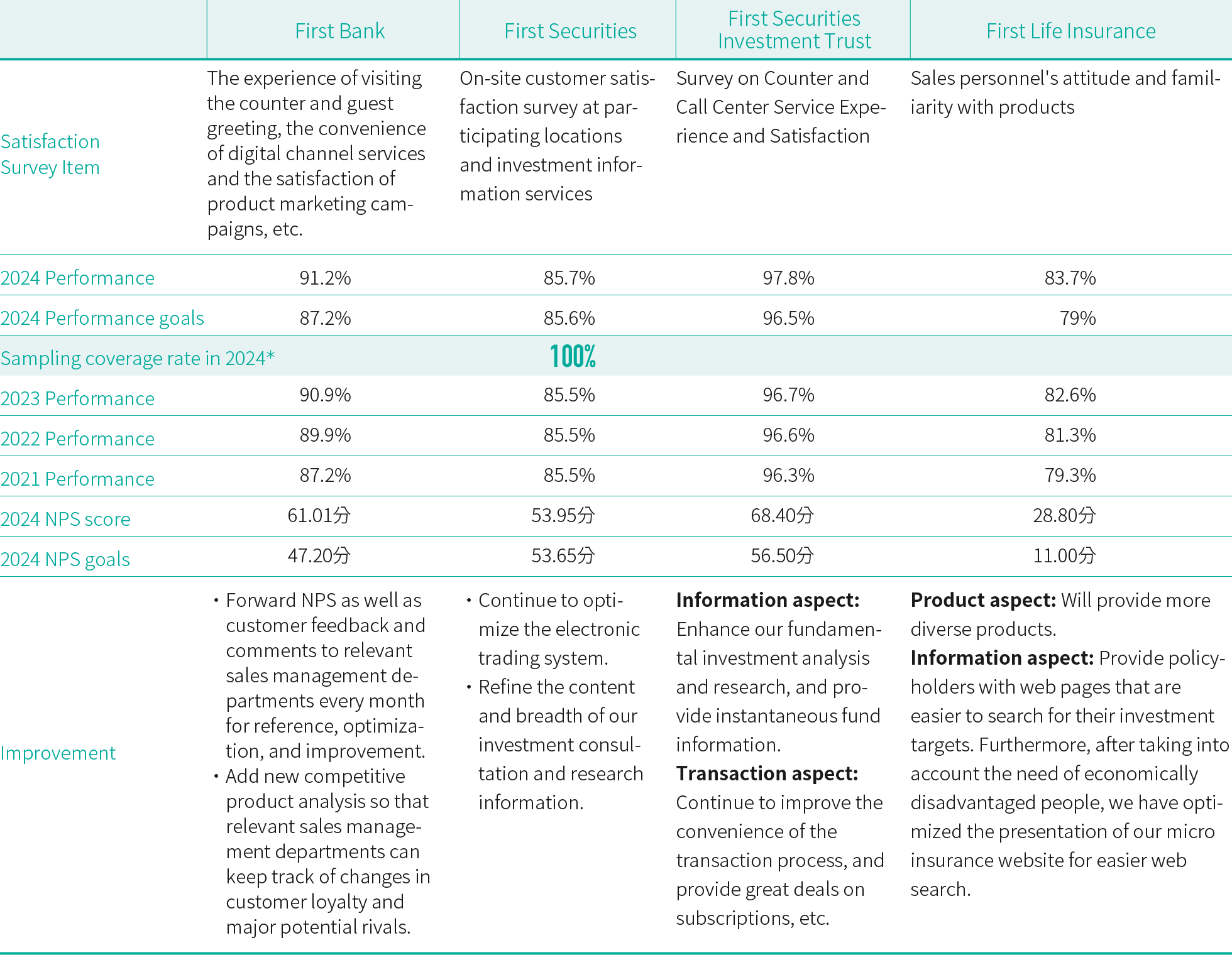

Customer complaints and satisfaction surveys

We value rating and suggestions for products or services by customers, every year we conduct complete sampling to savings, foreign exchange, credit, financial management, credit cards, insurances, securities, investments lectures, APP functions, etc and through phone calls, email surveys, activity pages, customer service or retaining market survey companies we conduct customer satisfaction survey, and since 2022 we has conducted an online satisfaction survey and disseminated information about fraud prevention to on-site elderly customers in order to protect their rights and provide a service more close to their needs. At the same time, we use Net Promoter Score (NPS) to count and relevant departments will conduct improvements on items of lower satisfaction scores and customer suggestions.

◎ Customer satisfaction survey of past years

*:The samples drawn by each subsidiary covers the main business of each such company, which is sufficient to infer the current status of the overall

active customers.

Moreover, a mechanism has been established to handle consumer complaints and disputes. Aside from formulating the "Operating Guidelines for Handling Customer Complaints" and procedures for handling various business disputes, First FHC also provides access to the online customer service of its subsidiaries, toll-free customer service phone numbers, dedicated phone numbers for business consultation, and complaint mailboxes under the "Stakeholder Communication" menu item on its official website. First Commercial Bank has also installed a 24 nours customer service hotline as well as an email box to remain in constant communication with its customers. In 2024, the Bank obtained the "AA" accessibility label for its official website and major e-banking services. In addition, it also enhanced its over-the-counter outreach mechanism for disadvantaged and elderly people as well as people suspected of suffering from dementia when they approached us for online banking, debit cards/voice-activated money transfer and foreign exchange operations. We also provided the "friendly reservation service", in addition to installing the "Senior Citizens & Friendly Service Hotline". To cooperate with the competent authority's policy to reinforce the review and evaluation mechanism for fair customer treatment, First Commercial Bank, First Securities, First Securities Investment Trust and First Insurance continued to refine their procedures for handling customer complaints in 2024. They regularly compile and sort major cases of customer complaints, and submit them to the Board. Customer complaints lodged with the Financial Ombudsman Institution are also regularly submitted to their respective Board of Directors for future reference, including the types, number, indemnity and handling status of such cases.

To effectively improve our operating procedures and reduce customer complaints, First Commercial Bank has incorporated the performance for handling customer complaints into the performance review of each unit, in addition to establishing a customer complaint review mechanism. Education training will be intensified for employees with poor attitudes, and units with repeated negligence are required to submit concrete improvement measures. Moreover, a dedicated customer complaint area has been created on the internal network, providing business units with information such as analyses on customer compliant cases and related statistical tables for their reference. We acquired ISO10002 "Customer Complaint Management Certification" in August, 2024 to improve the quality of our handling of complaint cases and align ourselves with international standards. The Group accepted and handled a total of 290 customer complaint cases via various grievance channels in 2024. In particular, we were notified of 208 of these cases via competent authorities (please refer to the appendix for more details: sustainable operation indicators). For most complaint cases, we were able to complete customer pacification and replies within the required timeframe. We also analyzed customer feedback and compiled related statistics in accordance with business types, before sending them to related units for improvement.

Customer Care Events

◎ 2024 Customer Care & ESG Engagement Events

Reaching the Next Pinnacle of Corporate Success Lecture

"First Commercial Bank Marches Towards 2050 Net-Zero Emissions Goal with Customers" Lecture

Investment & Money Management Lecture for Customers

Financial Planning Clinic Seminar

Customer care investment checkup seminar in rural communities

Investment & Money Management Lecture; Celebrity Money Management Class

Seminars and regular live broadcasts of financial management courses

The Group's financial institutions organized the "Be a Young, Anti-fraud Vanguard and Steer Clear of Traps" campus promotional campaign in association with the FSC.